This website uses cookies. By using this website, you agree to our Cookie Policy.

The Evolution of European CMBS 2.0

October 11, 2018Why Are The Latest Developments in European CMBS Important?

- During the past year, mainly as a result of advantageous pricing, CMBS has returned as a method of financing European commercial real estate and offers an alternative to bank lending.

- The CMBS 2.0 template is being subtly modified to import features from the U.S. market such as sponsor-favourable features, although these are balanced by investor requirements.

- For the first time since the European CMBS market was last active, the U.S. risk retention rules are applicable to some transactions and the cashflows are structured accordingly.

- In addition to CMBS, the European commercial real estate finance market is evolving to finance assets in other ways – for example, by way of innovative structured finance bond issuances, such as credit tenant lease financing, and “privately” through “loan on loan” financing.

Background

Following the financial crisis, the European CMBS market began to re-emerge in 2011 and issuance continued until 2015 (“2011-15 European CMBS”). During this time, the CMBS 2.0 principles were established.1 However in 2015, public issuance ceased as a result of factors such as the Chinese financial crisis and the possibility of Greece exiting the European Union. Subsequent to this, favourable pricing allowed the market to re-emerge towards the end of 2017 and continue at a steady pace in 2018 (“2017-18 European CMBS”).2

2011-15 European CMBS Features

Investor-driven features

In certain 2011-15 European CMBS, anchor investors stipulated features in respect of the controlling class and voting. For example, an anchor investor purchasing a vertical strip of classes of notes (with the intention to subsequently sell the junior classes) may not have wished to have a controlling class concept in the structure that could block the anchor investor’s voting wishes in respect of senior notes still held by it at a future date (see below for the discussion under “Controlling class”). In 2017-18 European CMBS, features perceived to be investor driven, such as the diversion of amounts payable to Class X noteholders, have emerged in the circumstances described under “The Return of Class X” below.

Tail period

2011-15 European CMBS introduced a longer tail period (i.e., the period between the scheduled maturity date of the underlying loan and the final maturity date of the notes issued by the Issuer) of at least five years. The longer period was introduced to allow sufficient time for workouts (protracted workouts had been experienced on legacy pre-financial crisis transactions) and has subsequently been retained in 2017-18 European CMBS.

Interest rate capping mechanisms

Because any interest rate hedging required to be entered into by the borrower would have expired, LIBOR or EURIBOR are capped during the tail period to mitigate the risk of increases to LIBOR or EURIBOR after the scheduled maturity date of the loan. This is also reflected in 2017-18 European CMBS transactions. Additionally, as a result of an increase in the weighted average note margin, interest payable to the most junior classes of notes may be capped (known as an available funds cap which was present in CMBS 1.0 transactions).

Note maturity plan

2011-15 European CMBS introduced the concept of a note maturity plan. In a note maturity plan, the special servicer is required to prepare a plan setting out various options with a strategy to be followed six months prior to the final maturity of the notes. This plan is then presented to senior noteholders for approval. If the senior noteholders do not approve any of the options, the trustee is deemed to have been directed to appoint a receiver and commence enforcement of the security over the assets. This tool is used to prevent a protracted workout and continues to feature in 2017-18 European CMBS.

Asset status report

The asset status report concept was introduced to 2011-15 European CMBS, whereby the special servicer is required to prepare a report within a certain timeframe of the loan becoming specially serviced. The report should include typical information on a loan workout such as the status of the properties and any updated valuations. The report should also set out the net present value analysis of the different options available to the special servicer (such as working out the loan or enforcing the security). The asset status report is viewed favourably since, in a special servicing situation, investors receive a significant level of information relating to the assets.

Controlling class and ad hoc noteholder committee

The controlling class concept is a feature from CMBS 1.0 transactions. The controlling class is usually the most junior class of notes outstanding, provided that (1) the outstanding principal balance of such class is not less than 25% of its closing date principal balance; and (2) a control valuation event has not occurred. A control evaluation event occurs if, broadly, the difference between (1) the principal amount outstanding of the relevant class of notes and all classes of notes below it; and (2) any “valuation reduction amount” of the loan is less than 25% of the principal amount outstanding (in respect of that class of notes). A valuation reduction amount is typically the excess of the principal amount outstanding of the loan over 90% of the most recent valuation.

However, the controlling class did not always feature in 2011-15 European CMBS, particularly in some of the earlier transactions. This was as a result of the then relatively recent financial crisis and the resulting onerous workouts taking place on legacy transactions (where a single controlling class could obstruct a loan workout, often in opposition to the wishes of the majority noteholders). An obstruction strategy that may be utilised by the controlling class is exercising its right to replace the special servicer. This issue may be mitigated by frequent valuations (which is beginning to be adopted in 2017-18 European CMBS), since the controlling class is determined by reference to the valuation reduction amount, the aim being to prevent a value impaired class from exercising disproportionate influence.

Transactions may also contemplate the appointment of an ad hoc noteholder committee to represent all noteholders. The servicer or special servicer, as applicable, may then consult with the ad hoc noteholder committee in relation to matters such as loan modifications. It may not be the case that an ad hoc noteholder committee (representing the general noteholder body) and a controlling class (a single class) will cooperate in a workout, so transactions may opt to restrict the coexistence of both (which may be an investor driven requirement).

2017-18 European CMBS Features

Financial covenants and change of control provisions

The loans in 2017-18 European CMBS are tending to reflect a more U.S. style sponsor approach to financial covenants which was not always a feature of 2011-2015 European CMBS. For example, in 2017-18 European CMBS, financial covenants do not apply upon closing of the transaction. Financial covenants (loan-tovalue, or “LTV”, and debt yield) do start to apply after a permitted change of control.3 However, prior to a permitted change of control, there is a cash trap for LTV and debt yield. The cash trap continues to apply after a permitted change of control. After a permitted change of control, if the financial covenants are not satisfied, the borrower may cure the breach by depositing sufficient cash into the equity cure account or prepaying the loan. However, such cure rights cannot be exercised on more than two consecutive loan payment dates for each financial covenant and not more than four times during the life of the loan. If the cure rights are not exercised, this leads to an event of default under the loan. A non-permitted change of control requires mandatory prepayment.

The return of Class X

Class X notes were featured in CMBS 1.0 transactions. The amounts due to Class X notes are paid from the excess of the spread payable under the relevant loan over the spread payable to the applicable bonds. At the outset of a transaction, these payments usually rank pari passu with payments due to the Class A notes. In some pre-financial crisis transactions that experienced protracted workouts, the Class X excess spread referenced the interest payable rather than what was actually received on the loan (this has been addressed in later transactions). The Class X notes also maintained a senior position in the post-enforcement waterfall. The negative effect of such provisions on other classes of notes which transpired in the workouts of historic transactions meant that Class X notes did not always feature in 2011-15 European CMBS.

2017-18 European CMBS have been more decisive in addressing the Class X note structure. In some transactions, if the LTV exceeds a specified threshold or the debt yield falls below a specified threshold, it will cause a Class X interest diversion trigger (despite the fact that a financial default covenant may not have been triggered by the change to the LTV or debt yield). This will consequently cause interest that was due to the Class X notes to be held back. Such diverted funds will, after a note acceleration or loan level failure event, be applied as revenue receipts to the waterfalls. The waterfalls will then switch payments due to the Class X notes, subordinating them to the other classes of notes.

In certain 2017-18 European CMBS, the abovementioned features in Class X notes are viewed by investors as counteracting the absence of day one financial default covenants. These features help to address the issues presented by legacy pre-financial crisis transactions in which the presence of Class X notes reduced payments made to other classes of notes.

Liquidity support provided by notes

An additional new feature4 is where reserve fund notes (“RFN Notes”) fund the liquidity reserve. The proceeds of the issuance of the RFN Notes are then deposited into a liquidity reserve, which operates similarly to a traditional European CMBS liquidity facility. The RFN Notes rank senior to the other classes of notes and, overall, rank senior in the transaction waterfalls in the same manner as a typical bank provided liquidity facility.

U.S. risk retention requirements

A new structuring consideration that has arisen in respect of 2017-18 European CMBS is the impact of the U.S. Risk Retention Rules5 which were not applicable to 2011-15 European CMBS6.

“Sponsor”

If an European CMBS transaction cannot avail itself of the safe harbor provision7, it must comply with the U.S. Risk Retention Rules. A scenario where the U.S. Risk Retention Rules may apply to European CMBS is where a pre-originated loan (the “Real Estate Loan”) is advanced by a U.S. credit institution. The U.S. credit institution is likely to fall under the definition of “sponsor” (primarily by virtue of it being chartered, incorporated or organized under U.S. law). The U.S. Risk Retention Rules generally require “sponsors” to satisfy the risk retention requirements for assets they securitize. 8. This means that the sponsor cannot rely on the safe harbor provision under the U.S. Risk Retention Rules.

The type of risk retention structure for the purposes of the U.S. Risk Retention Rules that is currently being used in European CMBS is an “eligible vertical interest” which has taken the form of a loan (the “Issuer Loan”) or an uncertificated trust interest (the “VRR Loan Interest”).

Definition of eligible vertical interest

In a securitization transaction collateralized by a commercial real estate loan, a sponsor may satisfy its risk retention requirements by retaining (or causing its majority-owned affiliate to retain) an “eligible vertical interest” in the issuing entity “in a percentage of not less than 5%”.

An eligible vertical interest is defined to mean a single vertical security or an interest in each class of ABS interests9 in the issuing entity, issued as part of the securitization transaction that constitutes the same proportion of each such class.

A “single vertical security” is defined to mean, with respect to any securitization transaction, an ABS interest entitling the sponsor to a specified percentage of the amounts paid on each class of ABS interests in the issuing entity (other than such single vertical security).

Structuring the eligible vertical interest

Eligible vertical interests may be structured such that a Real Estate Loan is sold by the sponsor in its capacity as the lender (the “Loan Seller”) to the newly formed bankruptcy-remote special purpose issuer of the securities (the “Issuer”). At the same time, taking the example of the Issuer Loan, the Issuer Loan is advanced by the Loan Seller (in its capacity as the “Issuer Lender”) to the Issuer.

On the issue date, (a) the securities issued by the Issuer will have an aggregate outstanding balance that is equal to 95% of the Real Estate Loan; and (b) the Issuer Loan will have an aggregate outstanding balance that is equal to 5% of the Real Estate Loan.

Under the terms of the Issuer Loan, the Issuer Lender has the right to receive 5% of all available funds (primarily comprising all principal, interest and prepayment fees received from the Real Estate Loan). This complies with the requirement described under “Definition of eligible vertical interest” above such that the sponsor has a percentage of not less than 5% of the amounts paid on each class of ABS interests in the Issuer.

Another option that has been used for the eligible vertical interest is for the Issuer to issue the VRR Loan Interest in the form of an uncertificated interest in a trust granted by the Issuer in favour of the Loan Seller (acting as a “VRR Loan Interest Owner”). The interest represents the right of the VRR Loan Interest Owner to receive a pro rata percentage10 of all amounts paid to noteholders.

The implementation of the U.S. Risk Retention Rules requires waterfalls to be carefully structured so as to ensure that available funds received from the loan are applied pro rata and pari passu as 95% to the securities and 5% to the Issuer Loan or VRR Loan Interest (as applicable). The 95:5 split is preserved before funds are applied to the tranching of the different classes of securities.

Disclosure to investors

The U.S. Risk Retention Rules have strict disclosure rules in respect of the prospectus or other offering document to be provided to investors in the securities. The disclosure is required to be provided to investors a reasonable time before the sale of the ABS interests. It is mandatory that there be a caption in the prospectus or other offering document entitled “Credit Risk Retention”. Under the caption, there is required to be a description of the form of the eligible vertical interest, the percentage that the retaining sponsor is required to retain as a vertical interest and a description of the material terms of the vertical interest and the amount that the retaining sponsor expects to retain at closing.

Compliance with European Risk Retention Rules

Under Regulation (EU) No 575/2013 (the “Capital Requirements Regulation”)11, the retention is required to be held by an entity that is an “originator”12, sponsor or original lender as those terms are defined for the purpose of the Capital Requirements Regulation. The definition of “originator” has two limbs, one of which is that the entity was involved in the original agreement that created the obligations being securitised. In 2017-18 European CMBS where the loans are pre-originated13, the loan sellers have qualified as originators within the aforementioned limb14.

Where there is dual compliant risk retention, the method of holding the retention piece as an eligible vertical interest for the purposes of the U.S. Risk Retention Rules, also needs to satisfy the retention methods that are permitted under the European Risk Retention Rules.

Article 5(l)(c) of Commission Delegated Regulation (EU) No 625/2014 (the “RTS”) provides that a retention in the form specified in paragraph 1(a) of Article 405 of the Capital Requirements Regulation (i.e. a retention of no less than 5% of the nominal value of each of the tranches sold or transferred to the investors) "may also be achieved by (…) retention of a vertical tranche which has a nominal value of no less than 5% of the total nominal value of all of the issued tranches of notes". The RTS requirement may be satisfied by virtue of the payment obligations of the Issuer under an eligible vertical interest, ranking pari passu with the securities and the Issuer being required to distribute all available funds from the loan proportionally between the securities and the eligible vertical interest on a 95:5 basis.

Credit Tenant-Lease Financing

In addition to the 2017-18 European CMBS transactions discussed above, there have been further recent notable real estate backed bond issuances, with one such example being the first credit tenant-lease financing transaction in Austria (as rated by Moody’s).15 In this transaction, the notes were backed by rental payments received from the State of Lower Austria in its capacity as tenant. The lease related to the parliament building used by the State of Lower Austria, and security was granted in respect of the rental payments (not in respect of the real estate). The rating of the notes depended on, among other things, the credit strength of the tenant.

The innovative structuring of the transaction drew on CMBS, sovereign debt and corporate secured debt features. This demonstrates that transactions may be structured without having to take security over the real estate asset. Instead, security taken over the rental income stream is a key factor. This is useful in a jurisdiction where the enforcement process may not be creditor friendly or the real estate asset is so bespoke that it would be difficult for creditors to sell the asset for an optimal price. For this approach to be taken, the tenant’s credit strength is crucial. The technique in this type of financing may be suited to fully fledged corporate businesses in addition to sovereign debt structures.

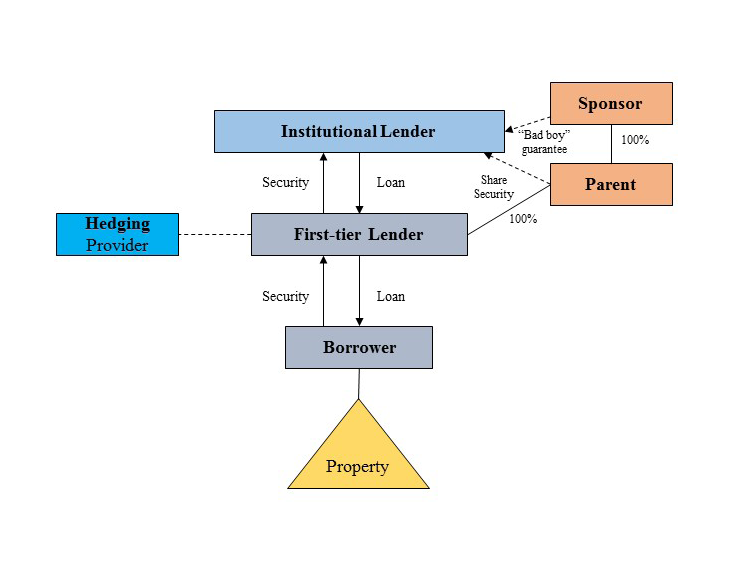

“Loan on loan” financing

In the context of this briefing, this financing technique refers to “private” transactions whereby institutional lenders advance loans to allow borrowers (“first-tier lenders”) to (i) advance loans to underlying borrowers; or (ii) purchase secondary market traded loan positions, both (i) and (ii) being secured over commercial real estate (“first-tier loans”). The first-tier lenders include start-up funds investing in real estate.

The loan provided by the institutional lender may be in the form of a warehouse which allows the first-tier lender to have financing in place at the outset thereby reducing the execution time for the completion of the financing to the firsttier lender’s underlying borrowers. The loan agreement between the institutional lender and the first-tier lender specifies that the first-tier loans are required to meet eligibility criteria and are subject to detailed due diligence on the underlying loans and real estate. There may also be features in the loan agreement, such as daily margining and mark-to-market requirements in respect of the real estate assets.

Reflecting the trend noted further above in respect of European CMBS, European “loan on loan” financing is also adopting sponsor features found in U.S. transactions. These features include “bad boy” guarantees which are provided by the sponsor to the institutional lender and are relevant in the context of discussions that take place in respect of the level of recourse to the sponsor.

It is important to consider aspects such as the securitisation treatment of the warehouse and the tax treatment of the first-tier lender. In addition, institutional lenders should request the provision of reports to them on the real estate that were commissioned at the first-tier level. Another consideration is who the addressees of such reports should be (this is also a consideration that is relevant to pre-originated CMBS transactions).

Inevitably, due consideration will be given to exit strategies for “loan on loan” transactions. Given the nature of warehouse financing, “loan on loan” transactions may require refinancing through the capital markets and there are different types of capital markets structures that may be adopted.

To view an example of “Loan on Loan” financing, please click here.

1 Market Principles for Issuing European CMBS 2.0 prepared by CREFC https://www.crefc.org/uploadedFiles/CMSA_Site_Home/Global/CMSA-Europe/Committees/European_CMBS_20_Committee/Market_Principles_for_Issuing_European_CMBS2.pdf

2 One such example is the BAMS CMBS 2018-1 DAC transaction.

3 A permitted change of control allows the loan sponsor to dispose of the entire portfolio without mandatory prepayment if there is, for example, (1) an IPO; or (2) a sale to an entity owning CRE assets with a minimum specified market value, provided that at the time of the sale: (a) an LTV test is satisfied; and (b) experienced property managers are in place.

4 See the FROSN-2018 DAC transaction.

5 Regulation RR, 12 C.F.R. §244.1, et seq.

6 The U.S. Risk Retention Rules became applicable to CMBS transactions on 24 December 2016. The European Risk Retention Rules have been in force since 2011. However, by virtue of the varying types of transactions in 2011-15 European CMBS, not all transactions were required to be EU risk retention compliant during that period.

7 Regulation RR, 12 C.F.R. §244.20.

8 The “sponsor” definition states that the sponsor “organizes and initiates a securitization transaction by selling or transferring assets, either directly or indirectly, including through an affiliate, to the issuing entity”. In a pre-originated CMBS structure, the sponsor will be selling or transferring the loan to the issuing entity.

9 An “ABS interest” is defined to include any type of interest or obligation issued by an issuing entity, whether or not certificated, including any security, obligation, beneficial interest or residual interest, the payments on which primarily depend on the cash flows from the assets owned or held by the issuing entity.

10 5% divided by 95%.

11 Under Article 405 of the Capital Requirements Regulation, European Economic Area (“EEA”) credit institutions and investment firms investing in securitisations are required to ensure that they will only be exposed to the credit risk of a securitisation position if the originator, sponsor or original lender has explicitly disclosed to the institution that it will retain, on an ongoing basis, a material net economic interest which shall not be less than 5%. Similar requirements apply to investments in securitisations managed by EEA investment managers subject to EU Directive 2011/61/EU and to investments in securitizations by EEA insurance and reinsurance undertakings.

12 As defined in the Capital Requirements Regulation.

13 “Pre-originated” in the context of this briefing meaning that a senior loan was advanced to the underlying borrower prior to the issue of the securities under the CMBS as opposed to an “agency” transaction where the proceeds from the issue of the securities are advanced on the same day to the issuer in its capacity as a borrower. Pre-originated transactions form the bulk of the recent issuance which is the first time that such structures have been used in such volume since before the financial crisis.

14 See further the EU Securitisation Regulation (Regulation (EU) 2017/2402) that comes into effect on 1 January 2019 and will amend the Capital Requirements Regulations as described in https://www.cadwalader.com/resources/clients-friends-memos/esmas-final-draft-disclosure-technical-standards and https://www.cadwalader.com/resources/clients-friends-memos/european-parliament-votes-to-adopt-the-securitisation-and-crr-amendment-regulations

15 https://www.moodys.com/research/Moodys-assigns-a-provisional-rating-to-CHF475-million-credit-tenant--PR_369283

{kind=link}