I. Market Momentum – Deal Volume and Lender Activity

As February comes to a close and we have all had a chance to digest Miami, our 2025 year-end and our prospects for 2026, it’s a good time to evaluate the state of our market. At Cadwalader, we have historically taken the lead on being the central data source for measuring the market, its size, growth, trends and challenges. Despite an ever-evolving macro-environment, the fund finance market has maintained a strong upward trajectory across several key dimensions, underscoring both the resilience of the sector and the intensifying growth and competition among lenders.

| Indicator | Recent Trend | Insight |

|

Deal‑volume momentum |

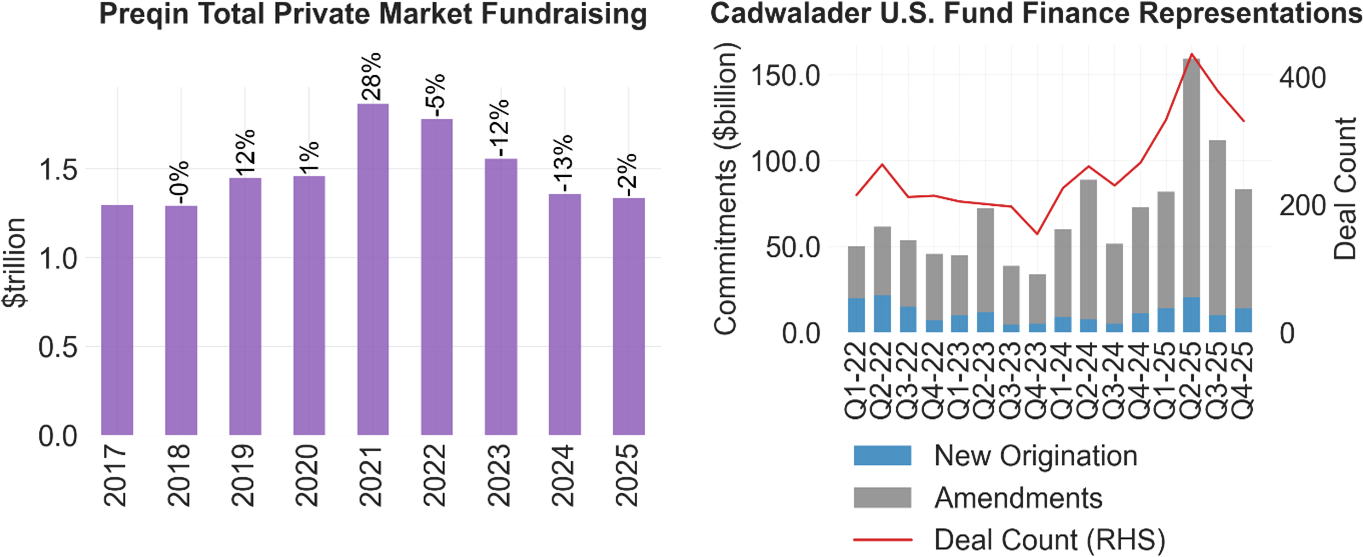

Even as fundraising levels remain depressed, deal volume has jumped 91% over the last three years. In Q2 alone last year, we saw originations surge to $19.1 billion in new commitments and $137.2 billion in extension‑and‑increase amendments, the highest new‑deal volume since 1H 2022. We saw new‑money subscription and NAV facilities rise by nearly $75.0 billion in 2025. The volume of amendments has also surged to capture more than 2/3 of deal activity. |

Deal flow is resilient. Even as fundraising plateaus, amendment activity and new money facilities continue to expand, driven by sponsor demand for liquidity and the “subscription‑plus” toolkit. Sponsors are leveraging existing capital to refinance and extend facilities, creating a steady pipeline of amendment work. |

|

Lender participation growth |

Cadwalader’s representation footprint expanded from 94 global clients in 2024 to 103 in 2025 (excluding ancillary participants). Lender participations have grown by 84 % over the last three years. But even so, most fund finance lenders still originate fewer than four new deals per year. The dedicated fund finance lender pool remains thin — there are just under 20 lenders that consistently originate and lead deals — but the health of the market is resoundingly expressed by the breadth of new and active participants that widened as banks re‑engaged after a 2023 contraction. |

The expanding client base reflects a healthier lender ecosystem, even as the market stays concentrated among the most relationship‑focused institutions. The relationships, depth of service and ability to adapt to sponsor needs remain a critical differentiator. The market’s competitive edge is driven by deep sponsor‑lender relationships rather than the sheer number of deals, rewarding institutions that can bundle ancillary revenue streams (fees, cross‑sell opportunities). |

|

Pricing dynamics |

In 2023, ~66 % of amendments involved a margin increase. By 2025, that pattern flipped — over 50 % of revolving‑subscription amendments saw margin cuts. The shift mirrors a “price‑rationing” environment where capital‑rich banks are willing to concede spreads to retain or win sponsor relationships. |

Pricing pressure is real. Margin reductions on amendments signal a market where lenders are aggressively courting business. Competitive pricing is benefitting sponsors, especially those seeking “subscription‑plus” structures (senior‑sub, term loans, flow participation, securitization). |

Exhibit 1: Fund Finance Growth Continues to Defy Fundraising

Source: Preqin and Cadwalader, Wickersham & Taft LLP.

II. 2026 Outlook – Poised for Growth

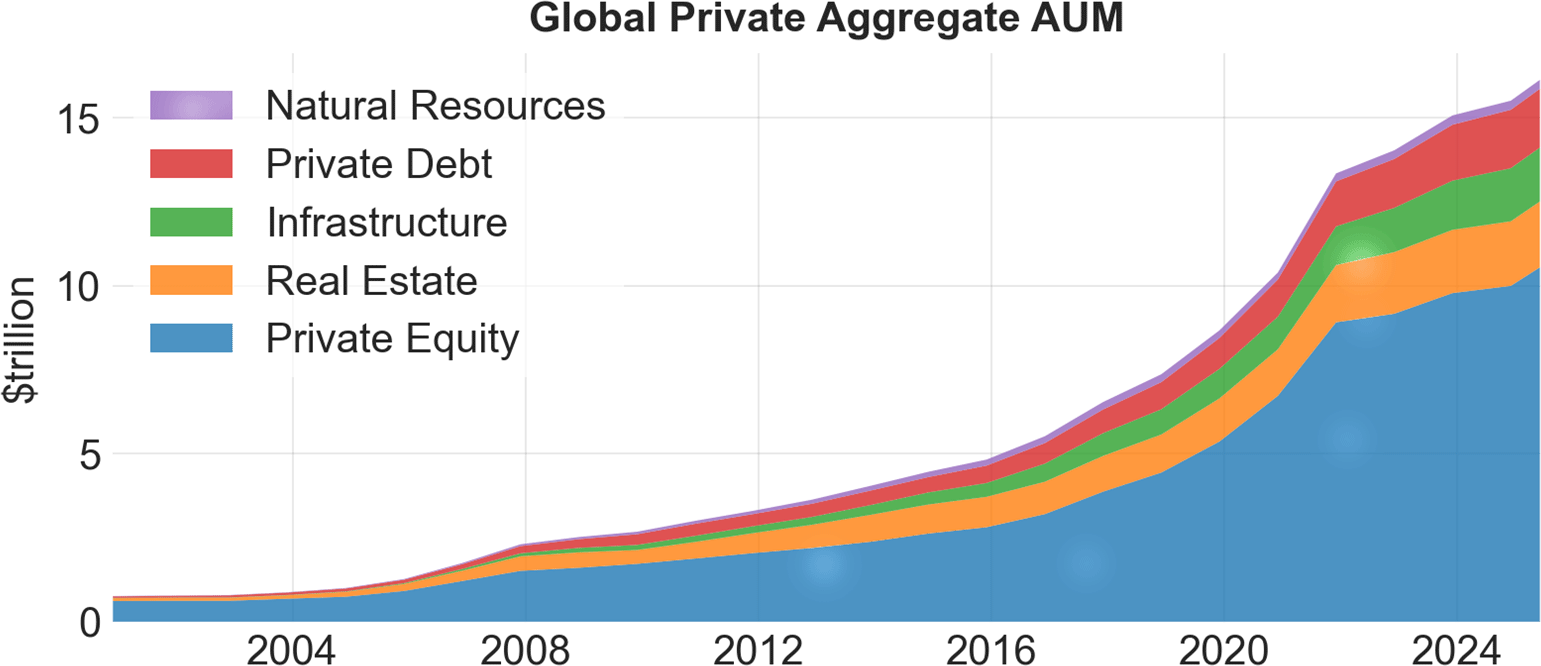

Together, these data points suggest that fund‑finance origination is poised for material growth in 2026, even as fundraising activity remains relatively down. We have seen the trends on the growth of new origination since this time last year. Non‑subscription, asset‑linked transactions now represent nearly double their share of the overall market over the prior five‑year period, underscoring a growing appetite for liquidity solutions independent of fundraising cycles. The private‑equity fundraising landscape is projected to stay within the $1.3–$1.5 trillion range. Total private market AUM exceeds $16.0 trillion, a level sufficient to sustain further NAV‑driven financing.

Exhibit 2: Private Market AUM Positioned to Support Continued NAV Expansion

Source: Preqin and Cadwalader, Wickersham & Taft LLP.

On the lender side, strong bank fundamentals and heightened competition creates a favorable environment for sponsors seeking flexible financing, while also prompting lenders to innovate on product terms and pricing. While the core U.S. GSIBs (global systemically important banks) continue to be programmatic originators, providing a stable backbone of capacity, we expect “subscription‑plus” structures—senior‑sub, term loans, flow participation and securitizations to pick up pace.

Collectively, these forces suggest that fund finance momentum will likely accelerate further in 2026, with sponsors benefiting from more competitive terms and lenders vying for deeper, relationship‑driven partnerships.

III. Competitive Landscape

Talent remains in high demand across all fund finance sectors; law firms, banks, and advisory boutiques are all expanding their fund finance capabilities to meet rising demand. Many are building dedicated securitization and structured‑risk‑transfer (CRT/SRT) platforms, allowing sponsors to tap off‑balance‑sheet capacity while preserving on‑balance‑sheet relationships.

Cadwalader Team Highlights – Growing with the Market

While the competition for talent is high and turnover rates are running above‑average industry‑wide, Cadwalader has risen to the challenge:

- All‑time headcount: The fund‑finance group entered 2026 at its largest size in firm history with more than 100 dedicated service professionals.

- Recruitment surge: More than 20 practitioners joined in 2025; 10 additional hires have been made in 2026, with the pipeline extremely active.

Our ability to attract top talent not only reinforces our market leadership but also ensures we can seamlessly cover every type of deal, from NAV‑based term loans to complex cross‑border securitizations across both U.S. and European jurisdictions. And, soon, we anticipate covering every type of deal in every time zone.

Cadwalader’s practice also continues to set the benchmark for structured‑risk‑transfer work.

We have:

- Led bespoke CRT transactions that blend traditional loan structures with innovative risk‑transfer mechanisms, giving sponsors flexibility to manage balance‑sheet exposure.

- Developed custom SRT solutions that allow investors to tranche risk in line with their appetite.

- Leveraged our transatlantic footprint to coordinate cross‑border financing and solutions for clients and sponsors operating in multiple jurisdictions.

These capabilities position us as a go‑to advisor for the most sophisticated fund finance and related structured deals and keep us at the forefront of market evolution.

IV. Closing Perspective

Fund finance activity has demonstrated resilience and growth despite a relatively static fundraising environment. The combination of record‑high amendment volumes, tightening margins, strong bank balance‑sheet capacity, and our deep talent pool positions Cadwalader to continue delivering innovative, full‑spectrum financing solutions for lenders and sponsors worldwide. While pricing pressure and regulatory change present headwinds, the firm’s transatlantic reach, deep expertise in securitization/CRT/SRT, and robust team make us uniquely equipped to help clients navigate the 2026 landscape. The state of the fund finance market is strong, and the overall outlook for 2026 positive and opportunity‑rich.

For a deeper dive into any of the trends or to discuss how Cadwalader can support your next financing transaction, please reach out to our Fund Finance team.