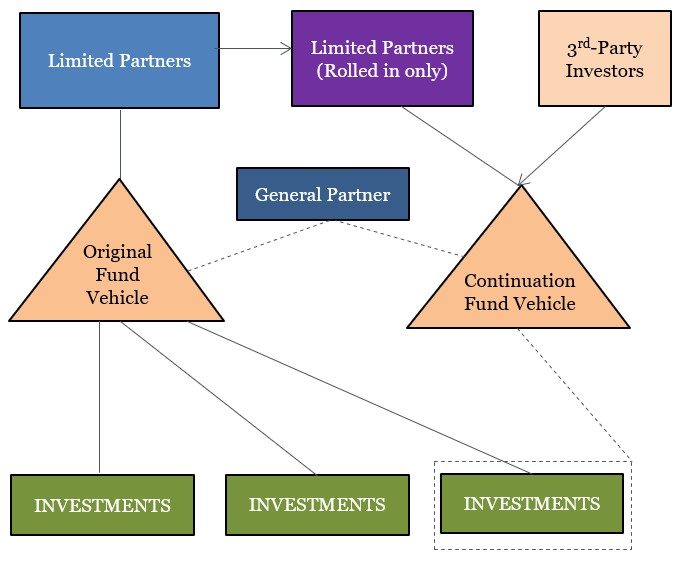

A continuation fund is an entity fund set up by a sponsor in order to purchase an asset (or assets) from an existing fund managed by that sponsor. There are a number of reasons as to why a sponsor would want to pursue this strategy compared with a third-party sale and a common consideration is that the existing fund is nearing the end of its term and the asset(s) subject to the sale may not reach the desired price in the current challenging exit environment and/or the sponsor and certain investors feel that the particular asset(s) are cash generative and are likely to increase in value with a continued hold by the sponsor combined with follow-on investments.

The establishment of continuation funds continue to grow in Europe against the backdrop of the exit environment, the level of interest rates, the vintage of certain flagship funds and pressure to make distributions to investors. The use of continuation funds is not limited to large-cap sponsors and many middle-market funds have established continuation funds in recent years to help address the challenges above.

With the increased prevalence of this strategy, there is increased focus on these vehicles (not least from regulators and investor bodies such as ILPA). Some of these considerations may be relevant to a lender lending to a continuation fund.

Structure of the Financing and Considerations

Security

As with typical subscription-line financings, the security package will usually include security over the continuation vehicle’s rights to call for uncalled commitments from its investors (and associated rights) coupled with security over the bank account into which the proceeds of such investor commitments are paid. However, with longer-term financings, it is common to see the continuation fund grant security over the interest it holds in the asset that it is purchasing.

Financial covenants

Given the special purpose of the continuation vehicle, the uncalled commitments financial covenants (the “UCC Test”) are typically slimmer than what would be seen in usual subscription-line financings. To help overcome the perceived risk of this (along with risks associated with single-asset/concentrated asset pool of a continuation fund), it is common to see a loan-to-value test that is tested against the value of the assets held by the continuation fund (an “LTV Test”). Some financings go a step further and also include an acquisition cost test to serve as an early warning trigger in respect of possible investor behavior.

Where there is an LTV Test, the concepts/definitions of Net Asset Value and Eligible Investments will be subject to similar consideration seen in NAV financings, but given the concentrated asset pool for a lot of continuation funds, there is typically a greater focus on the Material Investment Event concept in respect of the portfolio companies of an investment (which may result in an Investment ceasing to be an Eligible Investment for the purposes of calculating the LTV Test or lead directly to an Event of Default for single-asset continuation funds).

For longer term financings, it is common to see tiered covenants, whereby the LTV Test will be disapplied until a certain proportion of the investor commitments have been drawn from the investors with a corresponding step down in the UCC Test once the LTV Test has started to apply.

Cash sweep

The cash sweep/mandatory prepayment mechanics may either follow the approach for private equity NAV financings (where the continuation fund has a diversified portfolio of assets) or there may be an immediate 100% cash sweep of net proceeds arising from the investments (where the continuation fund has one asset or a concentrated pool of investments).

Due diligence

The extent of the due diligence on the assets subject to the purchase by the continuation fund will vary significantly between lenders (and will depend in large part on the extent to which the lenders are relying on the value of the asset(s) rather than the uncalled commitments of investors as well as the degree of the lenders’ familiarity with the asset(s) – frequently lenders are familiar with the asset(s) as a result of their participation in the financing of the selling fund and/or they are providing financing already elsewhere in the asset’s structure).

Additionally, the terms and timing of the acquisition by the continuation fund will need careful review given that the continuation fund is characteristically set up for a sole acquisition and those terms could be subject to various conditions which, if not fulfilled, prohibit the transaction (and ultimately release investors from their obligations).

Looking Ahead

The use of continuation funds are expected to continue to grow as it becomes a more established exit strategy (indeed, we are seeing a number of sponsors establish their first continuation fund(s) in the last year). In light of this growth, numerous prominent subscription-line lenders are exploring participating in continuation fund financings and we have also seen a number of new lender entrants committed in this space. With increased usage, greater attention from various bodies and publications is to be expected and may lead to more measures being enacted to address some concerns that these vehicles attract (such as conflicts of interests and transparency) which, in turn, will aid lender participation in this area of fund financing.