After three quarters of now more detailed reporting on bank lending to non-bank financial institutions, we’ve learned a few things about the loan category that captures fund finance loans for U.S. banks. Loans to nondepository financial institutions (NDFIs) is the fastest growing lending category to date in 2025 but also the cleanest, showing the lowest delinquency rate among major bank loan types.

Background

Banks first began reporting on loans to (NDFIs) in 2010, but the information value of the lending category was limited by its catch-all nature. NDFIs, under this single heading, included loans to insurance companies, mortgage lenders, business development companies, real estate investment trusts, marketplace lenders and private funds, among a range of other entities.

In 2024, call reports were updated to require banks with $10 billion or more in total assets to further group their NDFI exposures into specific: (1) loans to mortgage credit intermediaries, (2) business credit intermediaries, (3) private equity funds, (4) consumer credit intermediaries, and (5) other nondepository financial institutions.

Limitations

For the fund finance market, the newly detailed disclosure hinted at potential insight into the size, growth, and performance of the asset class, but its usefulness has been somewhat indirect. Because the NDFI subtypes are organized by counterparty rather than product, subscription loans can reasonably be grouped into several of the subtypes (e.g., private equity funds, business credit intermediaries, or other) and mixed in with other loan products.

Aside from this limitation, the first three quarters of reporting has involved significant reclassifications of loans, which means the early data should be handled with care. These reclassifications have affected what loans are included in the NDFI category—a number of banks moved C&I loans into the category, and some were also required to consolidate loans at foreign branches into NDFI. Banks have also changed how loans are classified within the NDFI subtypes with less reliance on the “Other” bucket in more recent quarters. These reclassifications are to be expected as part of the reporting transition phase, and can be controlled for in the future by measuring growth from a more settled point like the most recent quarter.

Observations

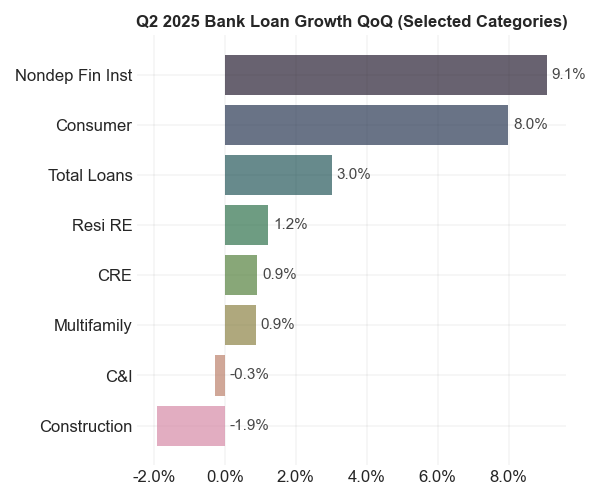

While NDFI data will not be directly applicable to fund finance, it nonetheless provides insight into the broader ecosystem in which fund finance exists. The first observation is that the non-bank lending remains one of the best avenues for sourcing loan growth in 2025. NDFI loans once again topped the list for loan growth among major lending categories in Q2 2025. As Exhibit 1 shows, banks with an NDFI strategy have been able to drive a differentiated loan growth profile.

Exhibit 1: NDFI Loan Growth Continues with Subtype Reclassificaitons Changing Mix

Note: We exclude certain specialty lenders from the bank data set.

Source: Bankregdata and Cadwalader, Wickersham & Taft LLP.

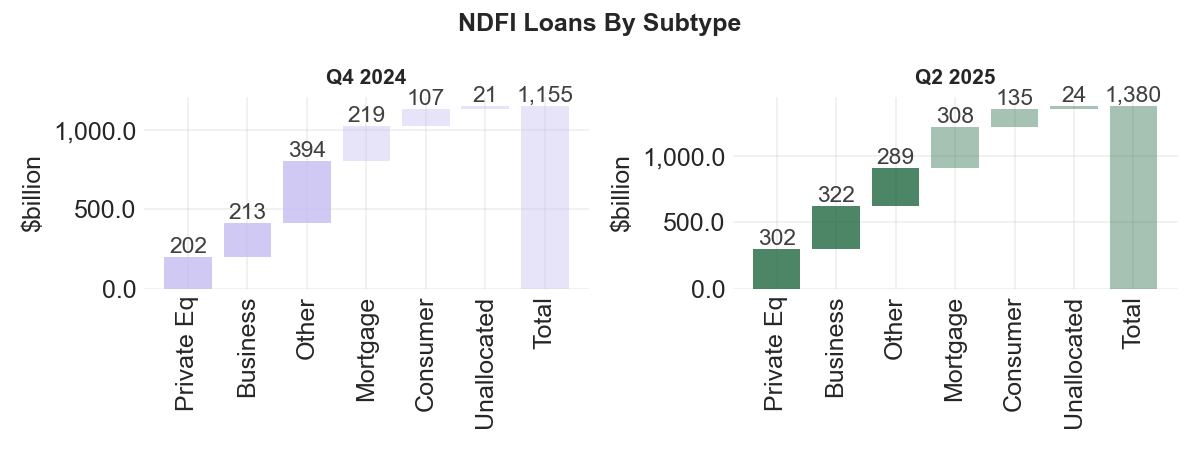

Within the NDFI dataset, loan grouping has moved around, with less reliance on the “Other” bucket over time, and hopefully arriving at a more stable order going forward. Reclassification within the category has been primarily driven by one institution. Because banks below $10 billion in assets are not required to disclose granular subtypes, we aggregate their NDFI exposure into an “Unallocated” category below.

Exhibit 2: Total NDFI Loan Growth Continues with Subtype Reclassificaitons Changing Mix

Note: Granular NDFI disclosure requirement applies to institutions with $10 billion or more in total assets. Where subtypes are not reported, we group loans into “Unallocated.” We exclude certain specialty lenders.

Source: Bankregdata and Cadwalader, Wickersham & Taft LLP.

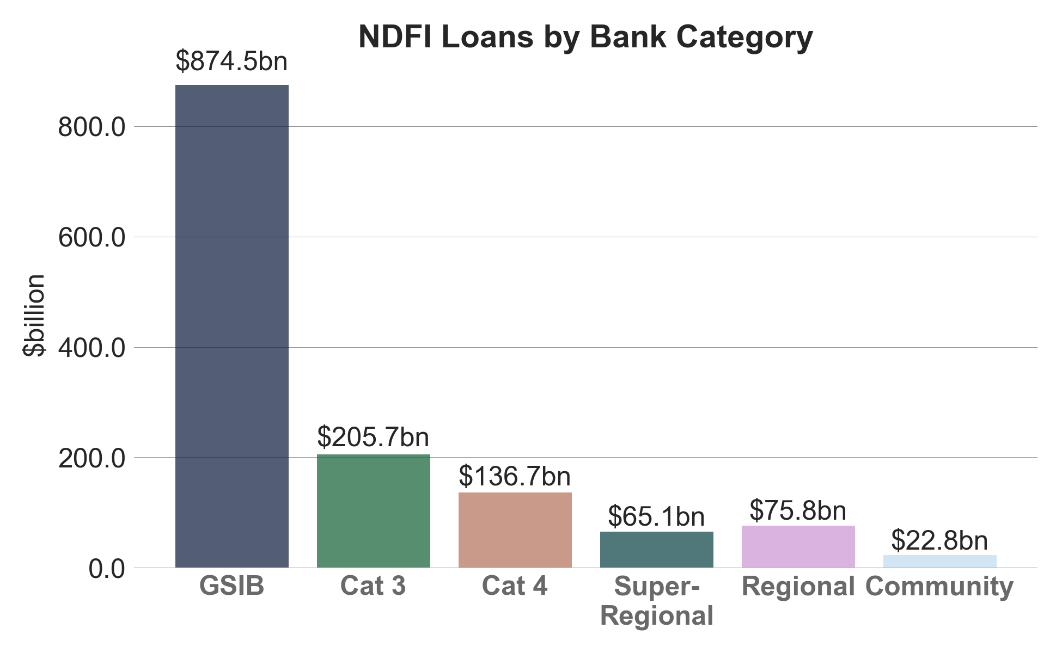

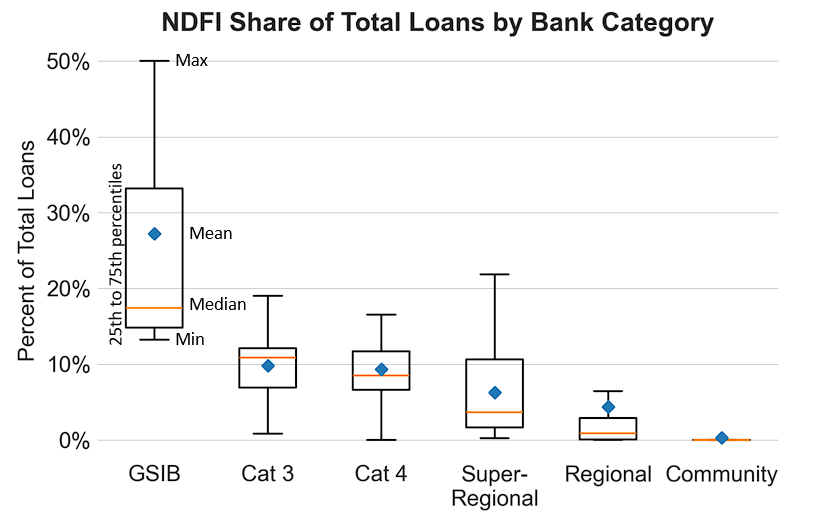

Large lenders appear to be more natural lenders to the non-bank lending space. The relationship is intuitive: These lenders are better positioned to provide a full suite of capital markets products that are relevant to fund sponsors. Rising sponsor concentration in the fundraising market has also translated to larger facility sizes, which work better on large balance sheets. GSIBs allocate a higher share of total loan exposure to NDFIs than other banks (Exhibit 4).

Exhibit 3: NDFI Loans Naturally Fit Large Lenders

Source: Bankregdata and Cadwalader, Wickersham & Taft LLP.

Exhibit 4: NDFI Loans Make Up a Larger Share of Loan Books for Large Lenders

Source: Bankregdata and Cadwalader, Wickersham & Taft LLP.

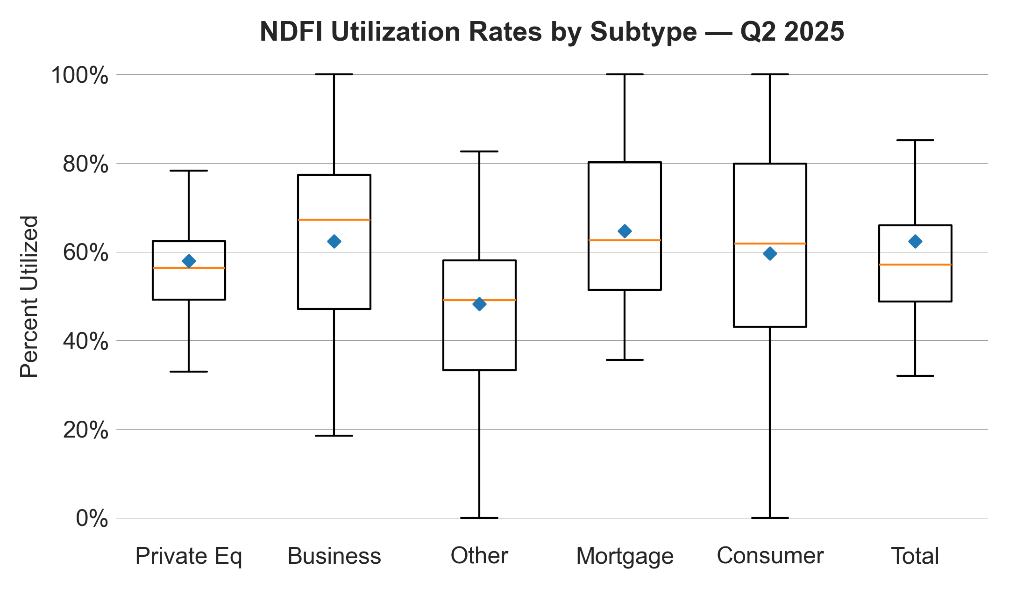

NDFI loan disclosures includes undrawn commitments, which provide the opportunity to look into utilization. Once again, the data organization by counterparty type rather than product type creates some limitations because most of the subtypes will include a wide range of instruments. That said, the private equity funds bucket may be more likely to consist of revolving loans. Consistent with that assumption, utilization rates in the private equity subtype are more consistent and centered around a mean of 51% (Exhibit 5).

Exhibit 5: NDFI Utilization Rates Are Clouded by Mixed Instrument Groupings

Note: Cert-level utilization = outstanding ÷ (outstanding + unused). Each bank cert counts equally (not balance-weighted). Includes banks with undrawn facilities (utilization = 0). Subtype coverage skews to larger filers given call report granularity rules.

Source: FDIC Research Information System and Cadwalader, Wickersham & Taft LLP.

Loan Performance

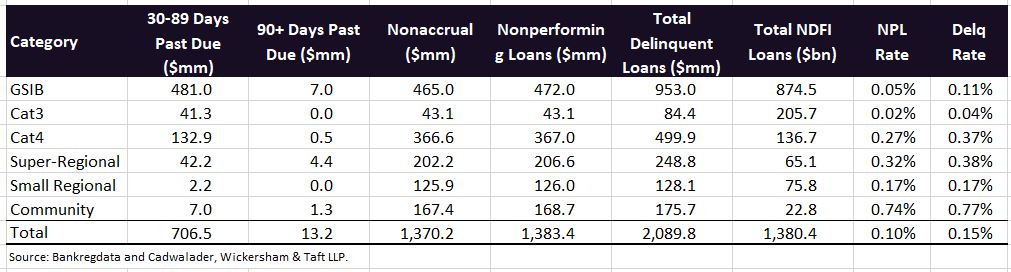

The rapid growth in NDFI loans continue to garner attention in many quarters. Some concern may be due to a lack of understanding of the impact of loan reclassifications on the sector, particularly around the implementation of the new disclosure standards in Q4 2024. More persuasively, loan performance for the sector is the cleanest among major bank lending categories. The non-performing loan rate (90+ day delinquencies plus non-accrual loans) stood at 10 bps at the end of Q2.

Exhibit 6: NDFI Loan Performance