On August 26, 2021, the U.S. Supreme Court issued an order vacating the Centers for Disease Control and Prevention’s latest eviction moratorium. Earlier this month the CDC issued an order banning evictions of residential tenants in counties experiencing high levels of community transmission of COVID-19, claiming that mass evictions would exacerbate the spread. The Alabama Association of Realtors, among other plaintiffs, applied to the Supreme Court to challenge this new moratorium. The plaintiffs had originally filed an action alleging that the CDC’s first eviction moratorium (which expired July 31) exceeded its statutory authority, and the District Court had agreed that the CDC lacked authority and granted the plaintiffs summary judgment to enjoin the moratorium. However, the District Court stayed its judgment pending the Government’s appeal to the D.C. Court of Appeals. When the plaintiffs then filed an emergency application to the Supreme Court to vacate the stay, the Court denied their application. Justice Kavanaugh concurred with the decision only because the then-current moratorium was set to expire in a few weeks. He warned that any extensions of the moratorium would require “clear and specific congressional authorization.”

When the CDC issued the new moratorium, the plaintiffs returned to the District Court, seeking to vacate the stay. The District Court agreed that the stay was no longer warranted because the Government was unlikely to succeed on the merits and because vaccines and rental-assistance distribution shifted the equities in the plaintiffs’ favor. However, the District Court was bound by the decision of the D.C. Court of Appeals to keep the stay in place. The D.C. Court of Appeals again declined to vacate the stay. The plaintiffs applied to the Supreme Court a second time to lift the District Court’s stay.

In a per curiam opinion, the Supreme Court vacated the stay, deciding that the CDC exceeded its statutory authority in issuing the moratorium. To promulgate the eviction moratorium, the CDC relied on Section 361(a) of the Public Health Service Act, which states:

“The Surgeon General, with the approval of the [Secretary of Health and Human Services], is authorized to make and enforce such regulations as in his judgment are necessary to prevent the introduction, transmission, or spread of communicable diseases from foreign countries into the States or possessions, or from one State or possession into any other State or possession. For purposes of carrying out and enforcing such regulations, the Surgeon General may provide for such inspection, fumigation, disinfection, sanitation, pest extermination, destruction of animals or articles found to be so infected or contaminated as to be sources of dangerous infection to human beings and other measures, as in his judgment may be necessary.”

The Government argued that based on the first sentence of the provision, the CDC has broad authority to take measures to control the spread of COVID-19, including issuing the eviction moratorium. The Court noted that this provision has rarely been invoked, and in the cases when it has been used, it was to quarantine infected individuals and prohibit the import or sale of animals known to transmit disease, not to justify an eviction moratorium. Specifically, the second sentence informs the grant of authority by illustrating measures that directly relate to preventing the interstate spread of disease by tackling the disease itself. Conversely, the CDC’s moratorium is much more indirectly related to interstate spread: “if evictions occur, some subset of tenants might move from one State to another, and some subset of that group might do so while infected with COVID-19.” The Court saw it as a stretch that Section 361(a) gives the CDC authority to impose an eviction moratorium.

Even if the text were ambiguous, the Court reasoned that the extremely broad scope of authority is an indication that Congress did not intend to grant such authorization. The moratorium covers at least 80% of the country, and the fact that Congress has provided almost $50 billion in emergency rental assistance illustrates the moratorium’s economic impact. Not only are the stakes financial, but the moratorium interferes with landlord-tenant relationships, a domain reserved for state law. The Court noted that precedents require Congress to enact “exceedingly clear” language if it wants to significantly change the balance between federal and state power and the power of the government over private property. Further, the criminal penalties (i.e., up to a $250,000 fine and one year in jail) imposed on those who violate the moratorium add to the over-expansive scope of authority. The Government’s interpretation of the statute places no limits on the measures that the CDC could take, and its claim of authority under such provision is unprecedented.

The Court further reasoned that the equities do not justify denying the plaintiffs the District Court’s judgment in their favor. The loss of rent with no guarantee of eventual recovery resulting from the moratorium puts landlords at risk of irreparable harm. Preventing landlords from evicting tenants who breach their leases intrudes on the right to exclude, one of the “most fundamental elements of property ownership.” While harm to landlords is increasing, the Government’s interests are decreasing, as the Government has had three additional months to distribute rental-assistance funds. Congress had notice that a further extension of the moratorium would require new legislation, yet it did not act in the several weeks leading up to the expiration of the moratorium. While the public interest in mitigating the spread of COVID-19 is indisputable, agencies may not act unlawfully to reach such goals. Thus, Congress, not the CDC, should be making the decision of whether the public interest warrants further action.

Justice Breyer, joined by Justice Sotomayor and Justice Kagan, dissented in the opinion. Justice Breyer began with the standard that the Court may not vacate a stay entered by a lower court unless that court clearly and demonstrably erred in its application of accepted standards. He concluded that it is “far from demonstrably clear” that the CDC does not have the power to issue the new moratorium. He disagreed with the majority that Section 361(a) does not grant the CDC authority to issue a moratorium − the statute’s plain meaning includes the moratorium as a measure that, in the agency’s judgment, is essential to contain disease outbreaks. The second sentence should not be read to limit the first but to expressly authorize inspections and other steps necessary in the enforcement of quarantines. He noted that it is undisputed that the statute permits the CDC to adopt significant measures such as quarantines, which arguably impose greater restrictions on individuals’ rights and state police power than restrictions on evictions. Further, the rise in COVID-19 cases tips the balance of equities towards leaving the stay in place, and the public interest is not favored by the spread of COVID-19 or a court “second-guessing” the CDC’s judgment. He concluded that the legal questions that have been raised about this federal statute call for “considered decision-making, informed by full briefing and argument” and the CDC’s moratorium should not be vacated in a summary proceeding.

With this decision, the District Court’s judgment will be enforceable, which means the CDC’s eviction moratorium is no longer in effect. Residential landlords may pursue eviction proceedings regardless of a tenant’s financial status impacted by COVID-19. We will keep you apprised of any further developments.

One of the standard tasks in real estate work is reviewing and analyzing tenant estoppels in connection with a potential loan or real estate purchase of a building with commercial tenants. A tenant estoppel is a signed certificate made by a tenant certifying for the benefit of a potential buyer and/or lender of a property that certain material terms of its lease are correct as of a certain date. Potential lenders rely on tenant estoppels for purposes of their underwriting and due diligence by taking into account representations from the tenant, such as the actual rent that is currently being paid, the amount of outstanding improvement allowances, whether any defaults, offsets or abatements to rent exist and expiration dates.

In May of 2021, the Illinois Court of Appeals (the “Court”) held that estoppels are enforceable against a tenant’s subsequent actions and claims. In Uncle Tom’s, Inc. v. Lynn Plaza, LLC (2021 IL App (1st) 200205 (May 21, 2021)), the plaintiff, Uncle Tom’s, Inc. (“Uncle Tom’s”), leased and operated a restaurant known as Market Square Restaurant in a strip mall owned by the defendant, Lynn Plaza, LLC (“Lynn Plaza”). Uncle Tom’s lease was set to expire in 2013, and in 2005, Uncle Tom’s attempted to exercise its 15-year extension option under its lease, but the parties could not agree on the square footage of the renewed lease for purposes of calculating base rent for the extension period. In 2011, Uncle Tom’s filed a complaint with the Circuit Court of Cook County (the “Circuit Court”) for declaratory judgment on the rent issue and also filed an equitable accounting claim for certain disputed amounts of common area maintenance (“CAM”) charges that Uncle Tom’s had paid to Lynn Plaza over the years. Uncle Tom’s complained that Lynn Plaza incorrectly charged and received certain CAM charges that were not included in the description of CAM charges under the lease. The disputed CAM charges were for management fees (billed and paid in January of 1998 for the year 1997) and easement charges for the use of a parking lot owned by a neighboring power company, which Uncle Tom’s had been paying for with CAM charges for almost 10 years. In July of 1998, in connection with a loan Lynn Plaza was seeking for the strip mall, Uncle Tom’s principal executed a tenant estoppel certificate representing to the proposed lender that “rent had been paid through July 1998” and that “there were no defenses to or offsets against the enforcement of the Lease or any provision thereof by the Landlord.” The Circuit Court granted summary judgment in favor of Lynn Plaza finding that Uncle Tom’s was estopped from challenging the disputed CAM charges based on the estoppel certificate its principal had signed.

The case came to the Court on appeal from the judgment entered into by the Circuit Court and the Court reviewed the estoppel issue de novo. Uncle Tom’s argued three points:

- Uncle Tom’s argued that the estoppel did not specifically mention the CAM charges at issue, so it could not be estopped for these CAM charges. The Court denied this argument reasoning that the lease specifically included CAM charges as additional rent and Uncle Tom’s certification was clear on the issue − that rent had been paid and that “there were no defenses to or offsets against the enforcement of the Lease or any provision thereof by the Landlord” (i.e., Lynn Plaza had not violated the lease by assessing these CAM charges). The Court went on further to hold that estoppels are not meant to include and capture every single provision of a lease, as it would be a tedious process for all parties and the statements are clear on their own.

- Uncle Tom’s also argued that it did not know of the CAM charges it would incur after July 1998 (the date of the estoppel), so it could not be estopped for charges it did not know about. This argument was based on K’s Merchandise Mart, Inc. v. Northgate Ltd. Partnership (359 Ill. App. 3d 1137 (2005)), where the Court held that a tenant was not barred from challenging the management fees assessed by its shopping center landlord because “the events prior to the execution of the estoppel certificate did not rise to the level that [the tenant] should reasonably have known of the management fee.” Here, the Court rejected Uncle Tom’s argument based on the K’s Merchandise case because of Uncle Tom’s “contemporaneous knowledge of the significance of the disputed charge at the time it executed the estoppel certificate.” Before Uncle Tom’s signed the estoppel certificate, Uncle Tom’s knew of the disputed 2018 CAM management fee charges for six months and the disputed CAM easement charges for almost 10 years. Uncle Tom’s even went further and hired an attorney to dispute the CAM charges for the management fees. The amount of the disputed CAM management charges was also $15,698, and this amount was specifically called out with a note flagging the item in the CAM reconciliation statement. The Court reasoned that this was not the same as the K’s Merchandise case because there, the tenant received the reconciliation statement two months prior to signing the estoppel and the charge was for $300 embedded in a line item. The level of knowledge was not the same.

- Uncle Tom’s lastly tried to argue that the doctrine of equitable estoppel was not applicable here because there was no showing of a “misrepresentation or concealment of a material fact” (or the fraud element of equitable estoppel). The Court agreed with the Circuit Court here that this case was not based on an allegation of fraud, but on the execution of the estoppel itself.

The Court ultimately concluded that Uncle Tom’s was in fact estopped from challenging the inclusion of the disputed management and easement fees in CAM charges. What we learn here from the Court’s holding, other than the fact that, yes, you can hold a tenant accountable for what it represents in its tenant estoppel, is that: (1) when a statement is clear, such as “there is no defense or offset,” every specific, single kind of offset/defense that can occur under a lease need not be called out, (2) lack of knowledge of facts may be a defense to being estopped, but when there is clear evidence of the knowledge, this defense will not cut it, and (3) fraud may be a defense to a claim of an estoppel. So there you have it: a real-life example of a tenant being held accountable in practice and “estopped.”

In Part Two of our series on limited recourse finance in the European real estate finance market, we look at the structural features.

Limited recourse structure can be achieved either structurally (which is the most common in real estate financing) or contractually.

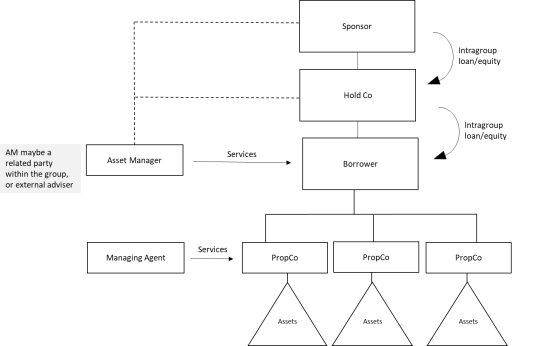

Typical limited recourse borrowing structure

In a typical real estate financing facility, as illustrated in the diagram below, a special purpose vehicle (“SPV”) is set up to be the Borrower and holds the underlying real estate asset; or, in the case of multiple properties, via subsidiary PropCos (each subsidiary again is set up as an SPV, only to hold the real estate asset). The Sponsor provides funding to the Borrower SPV either via an intragroup loan or by equity. A separate management company which is engaged to undertake the maintenance (and sometimes, manage the income such as rent and manage leases and tenants) provides services to the Borrower/PropCos with respect to the properties (“Property Manager”). Often, there is also an asset management company (generally an affiliate of the Sponsor) which provides investment and asset management advice to the Obligor Group with respect to the assets.

To achieve a limited recourse structure, only the Borrower SPV and its subsidiaries will grant security over its assets (which includes the underlying property). The Sponsor and Property Manager will not provide any security over its respective assets, save for assets/rights which are liabilities for the Obligor Group and therefore affect the solvency of the Obligor Group (examples include shareholder loans and claims under management contracts). This will be discussed in more detail in Part Three of this series next month.

Contractual terms to limit recourse – some limitations

Limited recourse can also be achieved contractually by having specific arrangements in place to ensure lenders only have limited claims over certain assets. However, this is often not the preferred approach, as enforcing contractual obligations in situations where the counterparty is not cooperative would require proceedings in court.

Furthermore, in ARM Asset Backed Securities S.A. [2013] EWHC 3351 (Ch), where the sponsor granted a share charge over an SPV, although the share charge provided that recourse to the sponsor is strictly limited to the shares of the SPV whose shares are charged, it did not preclude the Sponsor from being found to be unable to pay its debts and therefore can be wound up. Therefore, this judgment further puts into doubt the effectiveness of limited recourse only via contractual terms.

Clear distinction on assets and liabilities in or out of ring-fenced group

Given the recourse for the lenders is limited to the assets in the security pool and the Obligor Group (which is ring-fenced from the rest of the sponsor group), when conducting due diligence and constructing the security package, additional care needs to be taken to ensure these assets, upon enforcement, will yield sufficient recovery. To this end, in addition to the structural requirements in having all the assets supporting the loan sitting within the ring-fenced structure (or can be easily severed upon enforcement), one other key consideration for lenders is to ensure that liabilities and claims against the ring-fenced group are either contained within the group (i.e., intragroup liabilities) or, if such liabilities are outside of the group (most common example being sponsor debt), such liabilities can be severed in the same way upon enforcement. To the extent there are any liabilities outside of the group which pose as a threat to the lenders’ claim to the debt and/or the assets, such liabilities must be addressed adequately.

On June 29, 2021, in The Gap, Inc. v. 170 Broadway Retail Owner, LLC, the New York Appellate Division, First Department, overturned an earlier decision by the New York Supreme Court and issued a decisive victory to commercial landlords whose tenants have claimed that the COVID pandemic should be treated as a casualty under the terms of its commercial lease or that the COVID pandemic has frustrated the purpose of its commercial lease.

In the underlying complaint, The Gap alleged that the governmental shutdown of non-essential businesses was a casualty and, as a result, it was entitled to a rent abatement due to the loss of the use of all or a portion of its premises as a result of such casualty. The Gap further alleged that the landlord’s failure to permit a rent abatement as a result of such casualty was a breach of the underlying commercial lease.

The New York Appellate Division disagreed with these assertions and held that the casualty provisions of the lease “refers to singular incidents causing physical damage to the premises and does not contemplate loss of use due to a pandemic or resulting government lockdown.” Based on this definition, a pandemic and the resulting government lockdown is not a casualty, and, therefore, the New York Appellate Division dismissed the tenant’s breach of contract claim because the “[u]nderlying complaint fails to identify a single lease provision defendant allegedly breached, which is fatal to this claim.”

In another cause of action, The Gap alleged that it was excused from paying the rent due under the lease as a result of its inability to use the premises as a retail store due to an unanticipated event that could not have been foreseen or guarded against in the lease. The New York Appellate Division rejected this claim because the tenant was not completely deprived of the benefit of its bargain. In rendering this decision, the New York Appellate Division cited a case finding that the performance of a lease was not rendered impossible by reduced revenues. The court further dismissed this cause of action by finding that the brief closure required in the spring of 2020 was not a factor by the time The Gap filed its complaint and, as a result, determined that the tenant could not rely on the government-required closure to support its claims that it was impossible to perform under its lease.

In conclusion, the decision by the New York Appellate Division in The Gap, Inc. v. 170 Broadway Retail Owner, LLC strengthened New York law in protecting a commercial landlord from claims by a tenant that the COVID pandemic was a casualty under its lease or otherwise frustrated the purpose of the lease.

Substantive consolidation is an equitable remedy pursuant to which a bankruptcy court disregards the separate legal existence of a debtor, and pools the assets and liabilities of the debtor with one or more of its affiliates, in order to make distributions to creditors under a plan of reorganization or liquidation.

The Bankruptcy Code does not contain specific authorization for substantive consolidation. Instead, a bankruptcy court’s authority to substantively consolidate affiliated entities is derived from its general equitable powers.

When affiliated entities are substantively consolidated, intercompany claims among those entities are eliminated, the assets of the consolidated entities are pooled, and the claims of creditors against each entity are treated as against the common pool of assets. Substantive consolidation typically benefits one entity’s creditors at the expense of another entity’s creditors because each of the entities being consolidated has a different debt-to-asset ratio.

Lenders in structured finance transactions often require their Borrowers to be Special Purpose Entities (“SPEs”) to isolate the assets that are being financed, and the cash flow from those assets, from outside factors, such as the performance of other assets or the financial condition of the SPE’s affiliates. Substantive consolidation of an SPE with one or more of its affiliates defeats the isolation of the SPE’s assets, pulling them into a common distribution pool.

How it Works

To provide comfort as to the Lender’s interest in the assets being financed, and the cash flow from those assets, the Lender in a structured finance transaction often requires a non-consolidation opinion to be delivered by the SPE’s counsel at closing.

A non-consolidation opinion states that if one or more parent entities of the SPE files for bankruptcy, the bankruptcy court would respect the separate legal existence of the SPE and would not order the substantive consolidation of the assets and liabilities of the SPE with those of one or more of its parent entities, guarantors or affiliated managers (such as an affiliated property manager).

The opinion confirms that the SPE structure required by the Lender will be respected in bankruptcy, and that the SPE’s assets will remain isolated and will not be pulled into a common distribution pool with those of the SPE’s affiliates.

Because the Bankruptcy Code does not contain prescribed standards for substantive consolidation, judicially developed standards control. Bankruptcy courts have developed multiple, complicated and occasionally conflicting tests for determining whether an SPE should be substantively consolidated with one or more of its parent entities. However, four important categories of factors have emerged:

(1) Record keeping: the SPE should have separately identifiable assets and liabilities, and separate accounting records and financial statements.

(2) Operational issues: the SPE should be adequately capitalized and economically independent from its equityholders.

(3) Intercompany transactions: the SPE’s transactions with affiliates should be on arm’s length and commercially reasonable terms, and guarantees of the SPE’s obligations by affiliates and other credit support by affiliates should be limited.

(4) Benefits and harms: whether the benefits of substantive consolidation outweigh the prejudice to creditors that results from substantive consolidation.

Essentially, courts are looking to see whether the SPE’s assets and liabilities can be separated from those of its affiliates, and whether the SPE can conduct its business as a standalone entity. Courts also look to whether substantive consolidation would cause injustice to creditors who relied on the separate credit and existence of the SPE. Substantive consolidation may result where an SPE’s assets and liabilities are “hopelessly entangled” with those of its affiliates or where an SPE has to rely on its affiliates to conduct its business.

Practice Tips

The affiliates of the SPE that are included in the non-consolidation opinion are referred to as the non-consolidation opinion “pairings.”

- The rule of thumb, and the requirement in rated deals, is to pair the SPE against any equity owner (or group of affiliated equity owners) that owns 49% or more of the equity interests in the SPE, plus any guarantor and any affiliated manager (collectively, the “Related Entities”).

- The non-consolidation opinion will have the SPE on one “side” of the opinion, and the Related Entities on the other. Other deal-required SPEs, such as operating lessees or general partners of a limited partnership SPE, should be included on the SPE side of the non-consolidation opinion, paired against the Related Entities. No non-consolidation opinion is necessary between deal-required SPEs.

- In real estate transactions with both a mortgage loan and a mezzanine loan, the mezzanine borrower is not a deal-required SPE for purposes of the mortgage loan because it has separate debt that needs to be isolated from the debt of the mortgage borrower. Instead, the mezzanine borrower, as an equity owner of the mortgage borrower, should be included as a Related Entity in the mortgage non-consolidation opinion.

Here is a rundown of some of Cadwalader's recent work on behalf of our clients.

Recent transactions include:

- Represented the lenders in a $408 million CMBS financing in connection with the acquisition by an affiliate of KKR & Co. of HQ @ First, a three-building office complex in San Jose, California that is fully leased to Micron Technology, from Mori Trust Co.

- Represented the administrative agent on approximately $233 million of mortgage and mezzanine loans in connection with financing to reposition and reopen 9 select service hotels acquired out of bankruptcy.

- Advised the lender on a mortgage loan secured by two industrial parks in San Juan, Puerto Rico.

- Represented the lender in connection with the $215 million refinancing of 1450 Broadway by a Zar Group affiliate.

- Represented the agency lender under a transitional line of credit financing multifamily properties in the initial amount of $500 million, subject to increase up to $600 million, in connection with facility modifications, collateral additions located in Denver and Lakewood, Colorado, and additional advances.