Preferred equity − what is it? The question confounds many who encounter this unique and flexible financing alternative because it generally exhibits features of both debt and equity. The range of structures and terms for a preferred equity investment, which can often prove chameleon-like and result in inconsistent treatment and expectations by the preferred equity holder and others in the capital stack, makes it tricky to deal with if you are a lender considering making a mortgage or mezzanine loan to a borrower with a preferred equity investor. Whether you provide special recognition rights to the preferred equity holder may, in fact, come down to whether you consider preferred equity to be − or, just as importantly, must require it to be treated as − debt or equity, among a host of other considerations.

But, Really, What Is It?

Preferred equity is often described as either being more “debt-like” or “equity-like,” depending on whether its most prominent characteristics are more similar to debt or equity structures. At one extreme, a preferred equity investment can look almost like a mezzanine loan, in which the return on the preferred equity investment accrues at a fixed or floating rate, pays a guaranteed monthly coupon, includes a debt service reserve or deferred and accrued (or PIK) interest feature, is secured by a pledge of equity interests by other investors, and is characterized as debt for tax purposes. At the other extreme, though, preferred equity can be almost indistinguishable from any other investment in a joint venture, except that the preferred equity investor is entitled to distributions ahead of other investors in the waterfall and may remove and replace the manager, general partner or other control party of the joint venture for specified defaults or other causes. These extremes produce a range of variety in between, with very few market expectations for what preferred equity investments must look like.

At a basic level, however, a preferred equity investment occupies the space in the capital stack below mortgage and mezzanine debt, but above common equity. The investment is made through a joint venture structure (often a limited liability company or limited partnership that is a bankruptcy remote, special purpose entity) and the terms of the preferred equity investment are included in the joint venture’s organizational documents, as well as certain ancillary agreements. The return on the preferred equity investment (or at least some portion of it), as well as the repayment of the investment itself, will be paid ahead of distributions to others in the waterfall, and is due regardless of whether cash flow is sufficient to pay it in full. If the entire preferred equity investment is not repaid by a specified redemption date, or there are other defaults that remain uncured beyond notice and cure periods by the other investors, then the preferred equity investor will frequently be entitled to remove and replace the control party and receive distributions and exercise other remedies in order to “make itself whole.”

Special Recognition Rights

To ensure that the preferred equity investor’s exercise of remedies will not result in a default or other adverse consequences under any mortgage or mezzanine loan and without the need to seek consent from any senior lender, the preferred equity investor may seek special recognition rights from the holders of mortgage and mezzanine debt ahead of it in the capital stack. These special recognition rights may include the right to receive notice of defaults under the mortgage and mezzanine debt and an additional time period in which to cure defaults (beyond the notice and cure periods to which the borrower is entitled under its loan documents); the right to remove and replace the control party within the joint venture; the right to sell or assign the preferred equity investment to a third party, in each case, without lender’s consent or the payment of any transfer or assumption fee or triggering of an event of default under the mortgage or mezzanine loan documents; the right to remove and replace the property manager without lender’s consent; and/or the right to cause a sale of the property.

Lenders’ responses to requests for special recognition rights by preferred equity investors, as well as the form and substance of these special recognition rights, if granted, are often as varied as the preferred equity structures and terms themselves. At one extreme, with a more “debt-like” preferred equity structure, it would not be unusual for the preferred equity investor and mortgage and mezzanine lenders to negotiate and enter into a recognition agreement that is substantially similar to an intercreditor agreement between mortgage and mezzanine lenders and which contains provisions governing a UCC foreclosure of any pledge securing the preferred equity investment, additional cure rights, the requirement for replacement of guaranties by the preferred equity investor upon a change in control, and provisions governing the sale or transfer of the preferred equity investment to third parties. These recognition agreements also establish privity of contract between the preferred equity investor and other lenders, allowing the preferred equity investor to enforce its rights under the recognition agreement directly against the other lenders (and not indirectly through the borrower’s rights under the loan documents) in the event of a breach.

At the other extreme, especially with more “equity-like” preferred equity or where the parties have disparate negotiating leverage, senior lenders may refuse to deal with the preferred equity investor directly or at all, or opt to grant it any special recognition rights (or in certain circumstances, may even require that the preferred equity investment be expressly subordinated to the senior debt and the preferred equity investor agree to stand still). These lenders would argue that preferred equity is equity and should be treated as such and might agree to give the preferred equity investor courtesy copies of notices sent to the borrower, but no additional period in which to gain control of the borrower in order to cure defaults, and treat a change in control of the borrower as a permitted transfer only if allowed under the borrower’s loan documents.

Additional Considerations

Senior lenders may have other considerations in mind when deciding whether to extend special recognition rights to a preferred equity investor, or approving the preferred equity investment in the borrower in the first place.

For example, in a construction loan context, if the preferred equity is too “debt-like,” it may be a negative factor in the construction lender’s HVCRE (high-volatility commercial real estate) analysis, causing its construction loan to be categorized as an HVCRE loan. In such cases, to limit the construction lender’s HVCRE exposure, the construction lender may require that the preferred equity investment be restructured to have fewer “debt-like” features, if it permits the preferred equity investment at all.

Alternatively, if the preferred equity investment is being made by a strong institutional investor with experience comparable to the current sponsor in managing and operating commercial real estate, a senior lender may view the preferred equity investment as a net positive and even as additional credit support, especially if the senior lender is able to negotiate for replacement guaranties from a guarantor with reliable net worth and liquidity upon a change in control of the borrower.

Conclusion

Because there are no hard-and-fast rules about preferred equity, there also are no hard-and-fast rules about whether it must be accepted by senior lenders and, if so, how senior lenders must treat preferred equity investors. The range of how preferred equity investments are structured and their terms means that there will also be a range of how senior lenders respond to proposed preferred equity investments in their borrowers.

On September 2, 2021, New York Governor Kathy Hochul signed into law a new moratorium on evictions and foreclosures for residential tenants and small businesses. Recently, in the case Chrysafis v. Marks, the U.S. Supreme Court enjoined the enforcement of the previous residential moratorium in New York (which expired August 31), finding that the tenant’s ability to self-declare financial hardship while precluding a landlord from contesting that declaration violated the landlord’s due process rights. Additionally, in the case Alabama Association of Realtors v. Department of Health and Human Services, the U.S. Supreme Court held that the CDC exceeded its statutory authority in issuing its latest residential eviction moratorium and blocked the enforcement of such moratorium. In response, and citing the rise in cases due to the Delta variant of COVID-19, the New York legislature passed a new moratorium, which expires January 15, 2022.

The new law largely carries over the provisions of the COVID-19 Emergency Eviction and Foreclosure Prevention Act of 2020 (the “2020 Act”) and the COVID-19 Emergency Protect Our Small Businesses Act of 2021 (the “2021 Act”). The 2020 Act bans eviction and foreclosure proceedings against residential tenants who file a hardship declaration stating that the tenant is experiencing financial hardship due to COVID-19 or that moving would pose a significant health risk to the tenant because of a high-risk household member. Unlike the previous law, however, the new law allows landlords (and foreclosing lenders) to challenge the tenant’s hardship declaration. The modification was intended to address the Supreme Court’s due process concerns. Rather than telling tenants that “you cannot be evicted” until January 15, 2022, it says that “you may be protected from eviction until at least January 15, 2022” and provides landlords (and foreclosing lenders) an opportunity to request a hearing to determine the validity of the tenant’s hardship declaration. If a tenant files a hardship declaration, the landlord (and foreclosing lender) may request a hearing and make a motion attesting a good faith belief that the tenant has not experienced financial hardship, and the court must grant a hearing to determine whether the tenant’s hardship claim is invalid. After the hearing, if the court finds the hardship claim valid, the court will grant or continue a stay on eviction or foreclosure proceedings, provided that the court will direct, if the tenant appears to be eligible and has not yet applied, that the parties apply to the COVID-19 emergency rental assistance program of 2021 or a locally administered program to administer federal emergency rental assistance funds. If the court finds the tenant’s declaration to be invalid, the proceedings will continue to a determination on the merits.

Similarly, the new law provides eviction and foreclosure protections for small businesses, i.e., commercial tenants that are residents in New York, independently owned and operated, not dominant in their field and have 100 (previously 50 in the 2021 Act) or fewer employees. It prohibits eviction proceedings against a small business that has filed a hardship declaration stating that it has lost significant revenue or had significantly increased necessary costs during the pandemic. The new moratorium also prohibits foreclosure proceedings against small businesses that own ten or fewer commercial units if such small business files a hardship declaration. Commercial landlords and lenders may also challenge the small business’ hardship declaration in a hearing, and eviction and foreclosure proceedings will only be postponed to January 15, 2022, if the court finds that the hardship claim is valid.

We will continue to keep you apprised of any further developments.

In this Part 3 of the limited recourse financing series, we discuss some common issues and considerations with respect to the security package in a typical limited recourse structure.

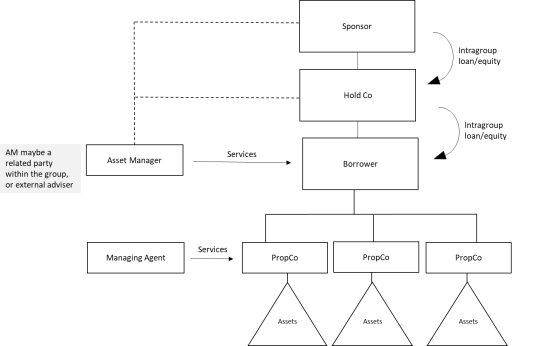

For a typical SPV structure (see diagram below):

The usual English law security package would include all asset security to be granted by all Obligors. The Obligors would include the SPV Borrower and, if the real estate is held by subsidiary PropCos, the shares of such PropCos and also all assets of such PropCos. This will include:

- Real estate mortgage over the Properties.

- Security over all bank accounts held by the Obligors. (This will also include the agreed control mechanisms. It is not unusual for certain bank accounts to be subject to the control of the lenders, requiring co-signing authority/approval before any withdrawals.)

- Security over insurances with respect to the Properties.

- Assignment of key (if not all) contracts, including the leases.

- Security over subordinated shareholder debt in the structure[1].

In addition to the security documents, the following documents are generally required:

- To the extent there is a property manager managing the property, a duty of care agreement between the lender, the property manager and the borrower.

- To the extent there is an asset manager, a duty of care agreement between the lender, the asset manager and the borrower.

- Subordination agreement with respect to the shareholder debt.

- To the extent there are any other key contracts which would affect the value of the income and/or the value of the property, additional documents which would provide the lender step-in rights (for example, if the property is a hotel and subject to a franchise or hotel management agreement with a hotel chain, a non-disturbance agreement).

In considering the security package, the ultimate question for a lender is how the security package should be structured to assist its exit strategy. Clearly, the cleanest, and possibly simplest, approach for a recovery strategy for lenders is to sell the property in an enforcement. Therefore, the approach taken in non-recourse/limited recourse real estate financing would often require security over all assets of the borrower SPV, and each intermediary holding company (if any) to the underlying asset, along with each asset that contributes to generating the cash flow to the property. To ensure the lender can sell off the entire package with relative ease, a share charge is often taken at the holding company level (over the shares of the Borrower SPV, and each of the entities that have property interest) to allow for a corporate sale.

To ensure the security package wouldn’t breach the non-limited recourse structure, security granted by the holding company/sponsor (namely, the share charge and security over shareholder debt, if applicable) must include limited recourse language. The language would provide that the lender's recourse is only limited to the asset subject to security (i.e., the said shares and/or shareholder debt), and beyond these assets, there is no further recourse to the sponsor in any way. Although the documentation seeks to achieve zero recourse/liability against the sponsor by limiting the lender’s recourse only to the assets, the sponsor could, despite the provisions of the security documentation, still be liable. This is the case where there is misrepresentation or breach of covenant on the part of the sponsor involved, as the lender may look to general contractual remedies against the sponsor for breach of contract and seek damages from the sponsor. However, this is distinct to recoveries for the underlying debt owed by the SPV borrower.

Aside from taking security over all relevant assets and cash generating contracts, lenders would ensure that anything which gives rise to liability would be addressed. The types of liabilities can be broadly split into two categories:

- liabilities which are essential to continue the day-to-day running of the property, and

- liabilities which were sunk costs into the SPV vehicle/structure and which, if removed, would not affect the future cash flow generated by the property.

Liabilities in the first category would include the head lease (if the property is a leasehold), ongoing maintenance/property management contracts, and, in the case of hotels, the franchise agreement − all of which are essential, and the loss of such contracts and related liabilities would be detrimental to the value of the property.

Liabilities in the second category would include shareholder loans and other subordinated debt, and depending on the nature of the asset management contract and the services provided, if it is determined such services do not contribute to the value and/or cash flow generated by the property, the liabilities under such contracts. It is often the approach to ensure that liabilities classified in category two can be eliminated in enforcement so that the asset is presented in as attractive light as possible to potential buyers.

In Part 4 next month, we will discuss some of the common pitfalls with limited recourse financing structures.

[1] It is often the lenders’ preferred approach to take security over the subordinated debt as it provides proprietary interest over the debt which makes it easier to discharge in an enforcement scenario. That said, in some circumstances where security cannot be provided over the subordinated debt, it is possible to agree to specific powers to write-off the subordinated debt in the subordination agreement. With this approach, the lenders will rely on its contractual rights under the subordination agreement.

Here is a rundown of some of Cadwalader's recent work on behalf of our clients.

Recent transactions include:

- Represented Bank of America, N.A. as lender in a $353 million mortgage loan to refinance One North Wacker Drive, a Class A trophy building in the Central Business District of Chicago.

- Represented the lender in a $259 million CMBS financing in connection with the acquisition of a newly constructed large multifamily property in the Miami metropolitan area.

- Represented the co-lenders in a $450 million refinancing of the Hyatt Regency Waikiki Beach Resort and Spa in Honolulu, Hawaii for Mirae Asset Global Investments Co., Ltd., which acquired the leasehold interests in the 1,230-key, full-service resort from The Blackstone Group L.P.

- Represented the lenders in a $685 million single-asset, single-borrower (SASB) securitized mortgage loan to refinance existing debt secured by a portfolio of 106 economy and extended-stay hotels that operate under the Motel 6 and Studio 6 brands.

- Represented the lenders in a $3.15 billion CMBS financing in connection with the acquisition of two resorts in Las Vegas, Nevada.