The fund finance markets have maintained their active pace into March without any signs of letup the last two weeks. Below are some of our recent market observations as well as some of my forecasts for the year ahead.

Transaction Volume. We completed our annual 2020 data project and analysis this week (if you are interested in the presentation, let us know). Among several areas where the data diverged from my expectations was our December activity levels: Even with the holiday break, December was our second busiest month of 2020, trailing only the tsunami that was March. Yet despite all the deals that closed in December (and it was a record month), our January and February activity levels have really held serve; our accruals have only moderated slightly off the December highs. Thus, our year-to-date activity levels exceed the corresponding period in 2020, and our deal sheet is running longer than last year at this time. It has been suggested that the market has felt disruption in the last two weeks, but our data suggests otherwise. We have not seen any impact on new deal flow or prospective matter accruals. Our number of new matters opened in the last week exceeds both our trailing 12- and 3-month averages. Our forward indicators, prospective hours accrued and LPA reviews, for the last two weeks are also in excess of trailing 12- and 3-month averages. Thus, we forecast a continued healthy deal flow into the second quarter. Longer term, we anticipate a very robust year for new fund finance origination. While growth rates will inevitably come down as the law of large numbers necessarily takes further hold, loan commitment and deal volume growth will remain outsized. Many indicators forecast fund formation to have a solid year, seeding opportunities. And virtually every bank is fully open for new business, many with recently increased product exposure caps. We think that on a market-wide basis, the positive momentum exceeds any headwinds, and the fund finance industry is likely to experience another year of sustained growth.

NAV-based Lending Market. The NAV and Pref Equity markets in Europe are accelerating, with much of last year’s chatter now materializing into live trades. Historically, the hit rate of prospective deals ultimately going under mandate has been relatively low. Currently, our EU team is seeing nearly all of their prospective deals move forward. We theorize that the COVID disruption helped many more European GPs familiarize themselves with their various financing and leverage options and, thus, this year they are executing. In the U.S., the wave of NAV-oriented rescue financings we discussed daily last April and May were virtually all shelved when the equities market rebounded in early summer. We continue to talk about NAV opportunities all the time, but the number of actual deals going forward remains lighter than we would have forecasted. While we think NAV financing in the U.S. will expand in 2021 and long term has significant growth potential, we think it will ultimately be more of a 2022-and-beyond story on our side of the pond.

“Revlon.” Many lenders have finalized their documentation changes to account for the recent “Revlon” ruling (if you need a primer on the issue, read our update memo here). I have this vision in my head of the UK looking at the U.S. and shaking its head in bewilderment …

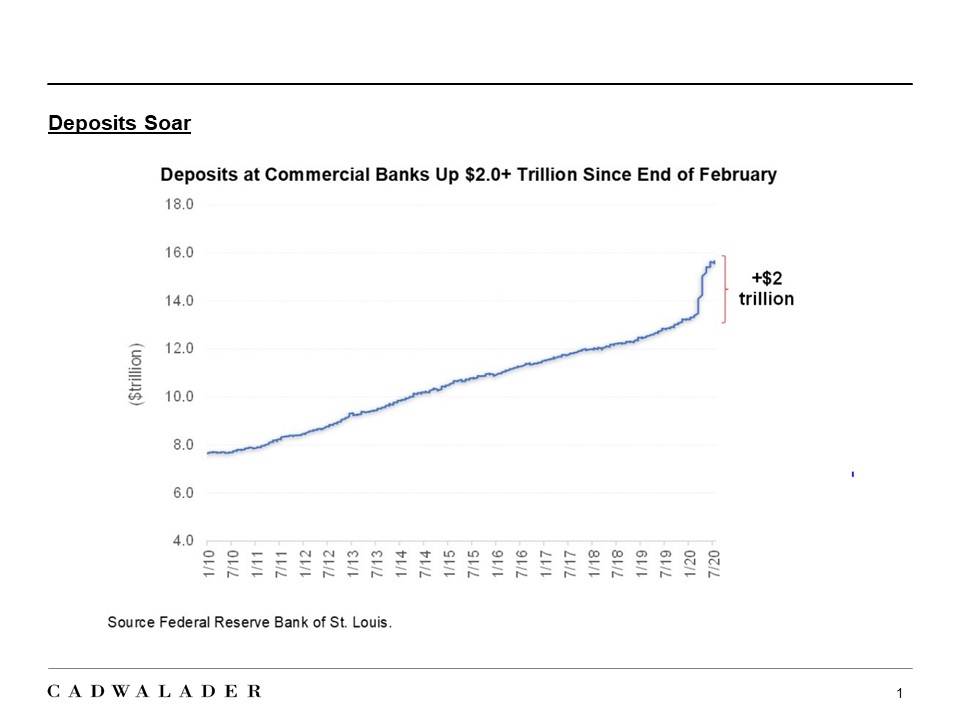

Hold Sizes. With President Biden signing the stimulus bill in the U.S. yesterday, an avalanche of deposits are about to land on the balance sheets of the U.S. banks that have large branch networks starting as early as next week. Check out the chart below that shows how deposit levels behaved in response to the 2020 stimulus payments. Upon receipt, banks will further develop their appetite to book assets. But booking assets at scale in many asset classes will require time and infrastructure investments. Subscription finance, however, offers efficient deployment at a relatively safe risk-adjusted return. Our expectation: We forecast bank hold sizes to meaningfully increase in 2021 as lenders look to efficiently book assets without having to make substantial corresponding investments. Hold size will also become more relevant in lead-bank selection. These trends will challenge the banks that rely on agent banks to feed them.

Utilization. The banks are going to hate this forecast; they have been working diligently the last few years to try and improve their portfolio-wide utilization. But I think utilization is going to tick down a bit in 2021, particularly for the banks whose books lean heavily into middle market private equity. First, even with the recent volatility, I think the equities markets are pricing optimistically. If fund sponsors share that view, bid/ask spreads will face some bridging challenges. Second, I think all the SPACs that came online last year are going to be more price-aggressive than PE and late-stage venture funds, especially as the year moves forward and they feel their deadline clocks ticking. While I think the overall impact of these issues will be modest on an industry-wide basis, I do think they will cause a slight constriction in PE deal flow. And hence could be an annoyance for many banks who see a few percentage points decline in their 2021 utilization.

ESG. I really think every bank needs its ESG-subscription finance product offering ready. Leaving aside that it would be a great thing if fund finance lenders could help push the world along in a more sustainable direction, I expect that many of the upper echelon fund sponsors will be asking for ESG-links in their facilities in 2021. If you get an RFP asking for an ESG-link, you want to be prepared and not caught scrambling. Wes Misson on our team is doing a terrific job advising lenders on ESG-related standards and methodologies if you need help getting started.

Recruiting and Retention. The combination of double-digit revenue growth with COVID-induced hiring freezes through most of 2020 led to a large portion of the fund finance market having to simply double down to get the deals done last year. And add to that a relative dearth of thank you’s for structuring deals that performed extremely well through a global pandemic and bonuses that in many cases were not well-linked to individual performance (but rather relatively muted because of challenges in other parts of the institution). When you overlay the underlying (overarching?) WFH fatigue that most everyone feels at times, I sense we are going to see high levels of employment transition in 2021. A lot of shops are hiring. Winning 2021 will require recruiting and retention successes.

Thank You. We at Cadwalader appreciate the trust and support of our clients and friends. If we can do anything to be helpful, please call.