Higher long-term interest rates complicate the sponsor value creation model by limiting the value that can be extracted from investment capital structuring due to higher term financing costs, undermining a buy-and-hold approach as lower benchmark rates at exit is no longer a given, and increasing the discount rate for asset net present value of investments. We see several potential implications for fund finance resulting from the 2026 rate environment:

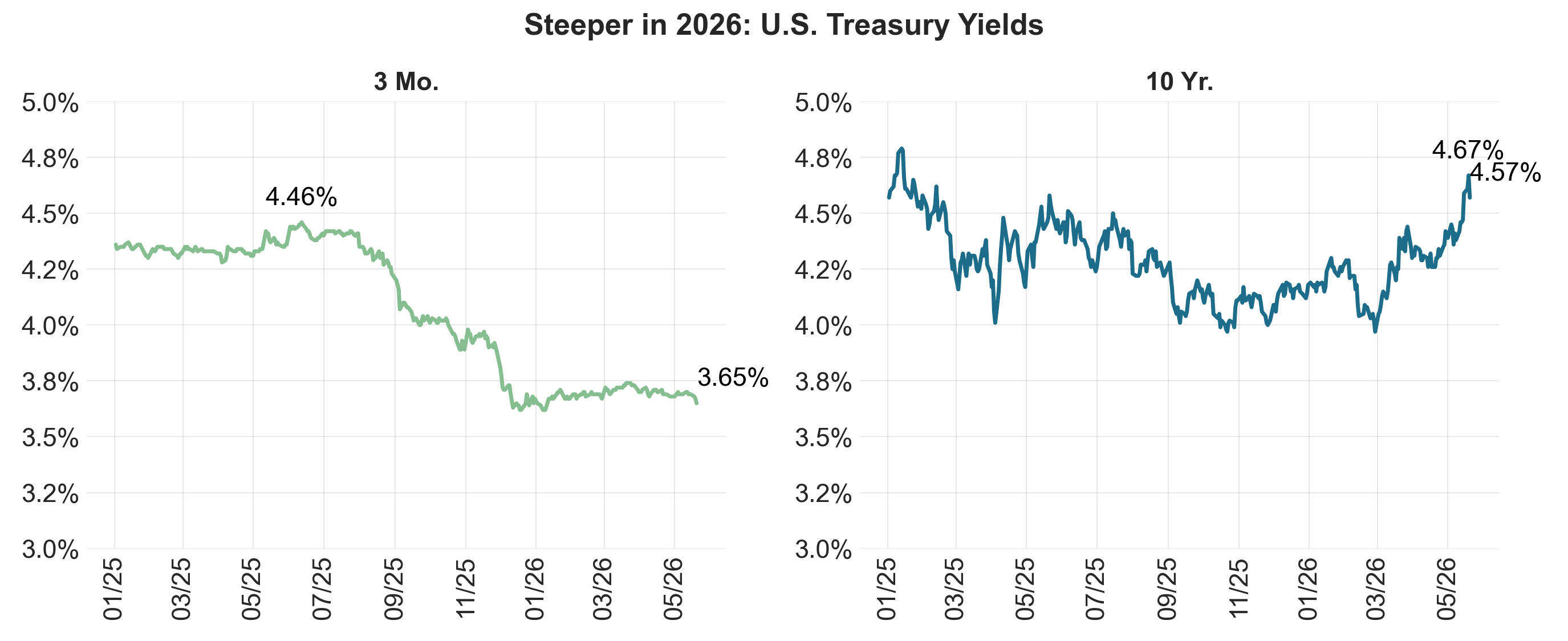

- A steeper yield curve means borrowing at the short-end of the curve, including via subscription and asset-backed revolving capacity, has become significantly more compelling for sponsors.

- Expect selective substitution away from longer-tenor fund-level debt to result in subscription amendment activity skewing toward reserving or increasing borrowing capacity, extending a trend that emerged in 2025. Look for facility utilization to increase at the margin. Overall bank balance sheet capacity has evolved to accommodate fund needs.

- Sponsors that seek to maximize short-end borrowing capacity may have more reason to explore umbrella and master facilities to consolidate borrowing capacity across funds.

- While long-duration, deep j-curve PE funds face fundraising headwinds due a long cash flow duration profile and a compressed risk premium between the 8% pref return and higher Treasury benchmarks, income-oriented fundraising may benefit, given a shorter duration profile and the ability to originate into a higher rate environment.

A Curve Steepening Recap

Yield curve steepening in 2026 doesn’t require commentary from FFF, but I’ll put a few observations on the table: (1) Steady front-end rates underscore that this is not a cuts-are-coming steepener, (2) higher long-end yields may be indicative of reduced appetite for duration, (3) term premium, the incremental compensation for holding longer exposure is clearly higher, (4) higher long-end rates reflect a mix of fiscal-driven (non-transitory) supply, inflation, and required risk premium factors.

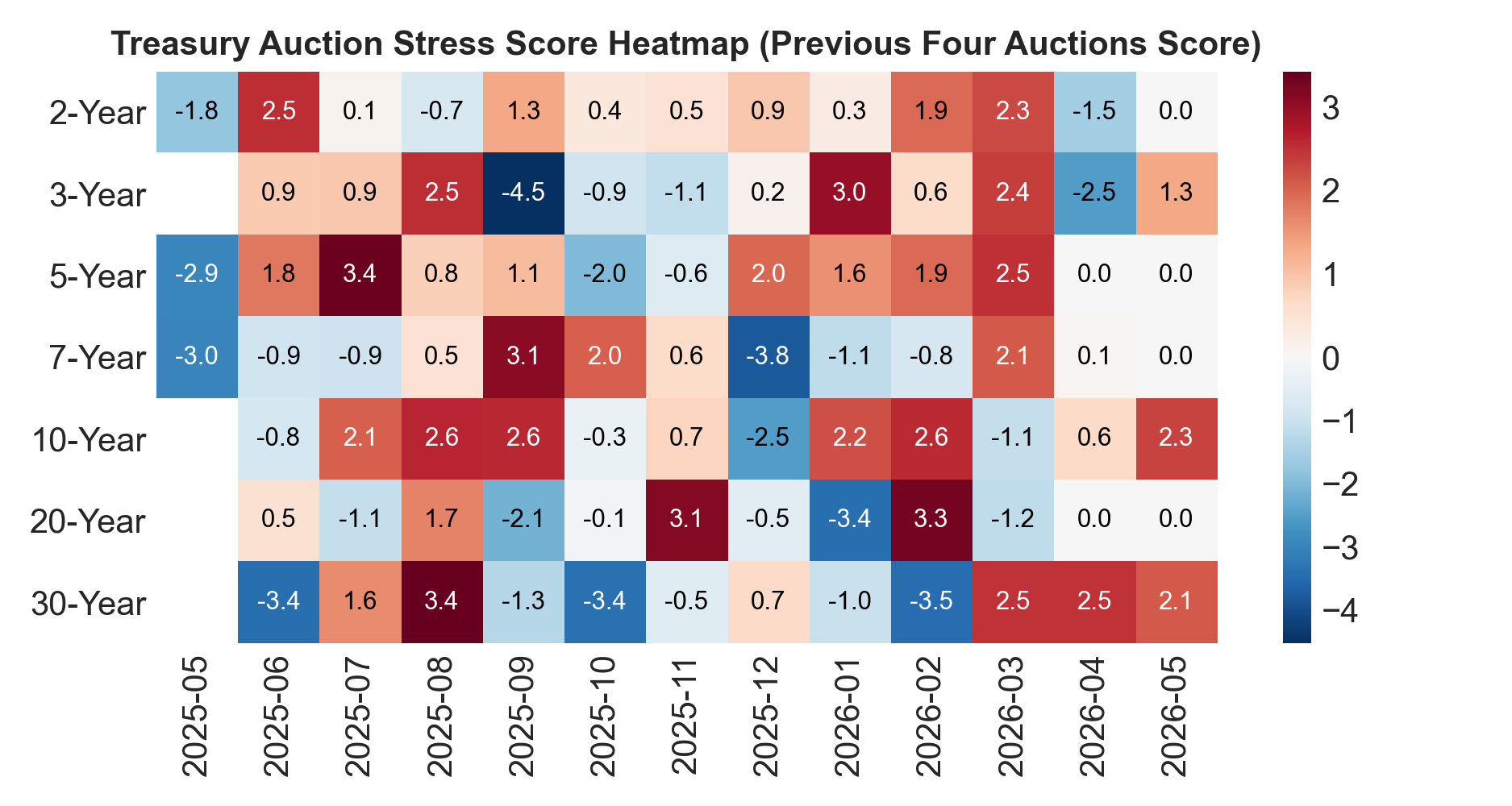

Source: U.S. Department of the Treasury and Cadwalader, Wickersham & Taft LLP.

Embedded in the higher yields shown above is a weakening demand picture that emerged in February and appears to be extending into May. Below we show a monthly tenor-bucket composite auction stress score matrix that measures Treasury coupon auction results against the prior four auctions. Higher stress score numbers this month (shown in red) signals weak support for long-end Treasury auctions.

The score combines four standardized auction components computed over a trailing four-auction window: a lower bid-to-cover raises the score, higher primary dealer takedown raises the score, lower indirect bidder share raises the score, and higher allotted-at-high raises the score. Higher yields should be viewed in the context of the weakening demand backdrop.

Source: U.S. Department of the Treasury and Cadwalader, Wickersham & Taft LLP.

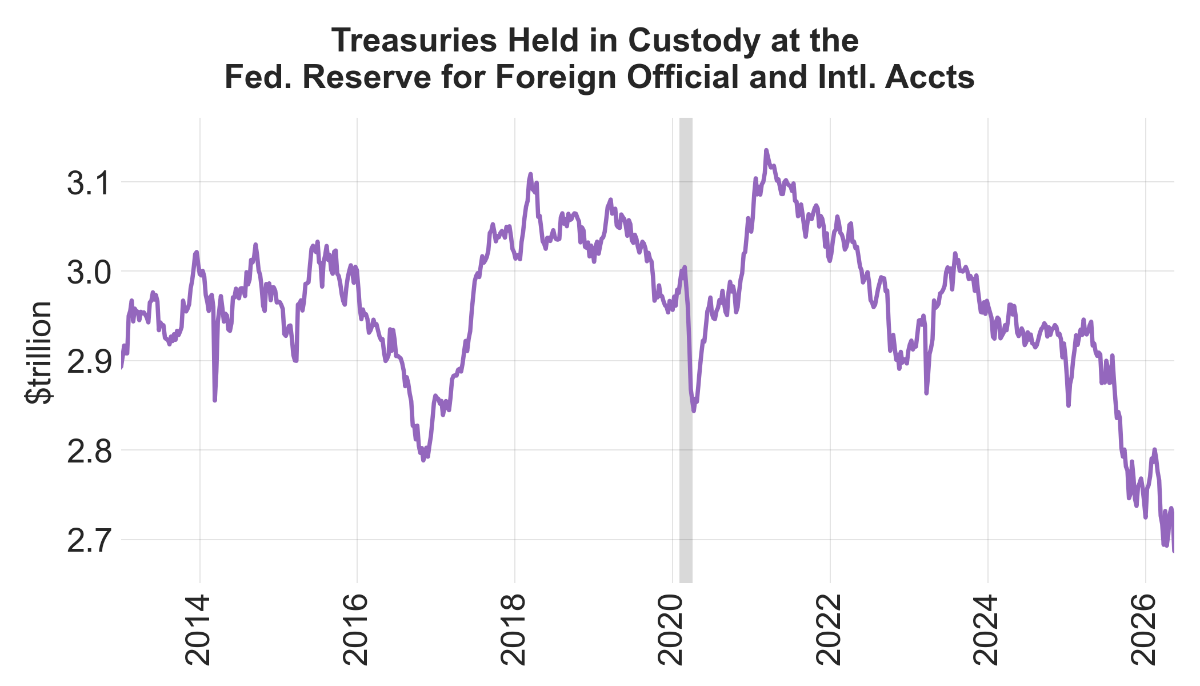

Part of the weakening demand traces to foreign buyers, as reflected in the decline in Treasuries held in custody at the Fed on behalf of foreign official accounts. As these generally price-insensitive, policy driven buyers have stepped back, auctions have come to rely more on price-sensitive buyers.

Source: Federal Reserve and Cadwalader, Wickersham & Taft LLP.

Foundations

Two foundational finance principles bear a passing mention in the rate discussion. First, higher discount rates imply lower NPVs. Reflexive surface-level commentary often dismisses the impact on the assumption that input cost disruptions may prove transitory, but this overlooks the elevated Treasury supply outlook and the soft demand picture discussed above, which are also priced into the yield.

Second, over time interest rates drive capital flows. Specifically, capital tends to flow away from slower-to-reprice assets with compressed risk premiums versus benchmark rates and toward more responsively-priced assets. Secondary fixed income securities tend to benefit early as discount accretion and curve rolldown opportunities become available while other markets reprice overtime with more gradual price discovery.

Fund Finance

Does all this matter for fund finance? Yield curve steepness well in excess of unused fees should make borrowing at the short-end of the curve via subscription and asset-backed revolving capacity more compelling to sponsors.

This already became visible in 2025 when 35% of the subscription amendments we processed included a commitment increase, up from 25% over the prior three years. The trend continues in 2026 with 30% of amendments to date including a commitment increase. Roughly 60% subscription amendments so far in 2026 have maintained or increased commitment size, showing that sponsors are biased to preserving or increasing subline capacity.

To be clear, this is not an argument for broader subscription adoption. Instead, the hypothesis is that a steeper yield curve will drive a marginal increase in subscription facility utilization, upsized commitments, extensions, and the use of umbrella structures to pool borrowing capacity across funds. The effect should be weaker for mature funds, where NAV or hybrid facilities remain the more natural liquidity tool.

Two Final Points

Optionality inside and outside the fund finance credit agreement continues to prove valuable: The sponsor-lender relationship allows for market-responsive changes to the commercial agreement.

As it relates to the broader environment, higher long-end rates pose a headwind to fundraising, particularly for equity funds given the duration profile, as the risk premium of the static 8% pref return is compressed by higher Treasury yields. At the same time, income-oriented fund asset classes (a smaller segment of the market) become relatively more attractive given the ability to originate into higher rates and benefiting from a shorter duration cash flow profile.