The first round of U.S. quarterly bank call reports for 2026 provided several notable datapoints for fund finance lenders:

- C&I bank may be entering a durable uptrend as banks regain share from private credit and regulatory capital revisions line up to add support.

- We read increased momentum in C&I as a positive signal for overall commercial lending appetite and as an indicator of support for the sponsor ecosystem.

- NDFI lending data appears to have moved through the reclassification noise of prior quarters, and growth in the segment continues.

- Within this category, lending to business credit intermediaries ticked materially higher during the quarter, likely pointing to liquidity demand at private credit borrowers translating to revolver draws.

Solid Loan Growth and Continued NDFI Expansion

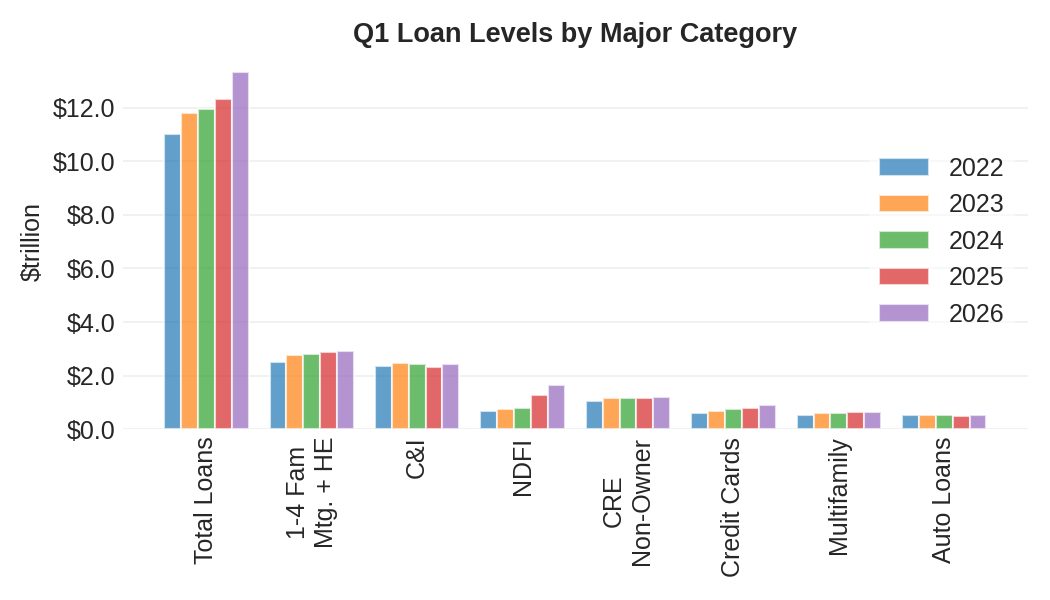

We saw plenty in Q1 call reports to validate our growth thesis for 2026, but longer-term shifts in bank lending are also becoming apparent. Notably, total U.S. bank loans on balance sheet grew at a 6.8% annualized rate during the quarter to reach a record $13.31 trillion (Exhibit 1), consistent with our view that capital, funding, willingness to lend, and credit conditions would support growth.

Exhibit 1: Loan Portfolios Expand Across Major Categories

Source: Bankregdata and Cadwalader, Wickersham & Taft LLP.

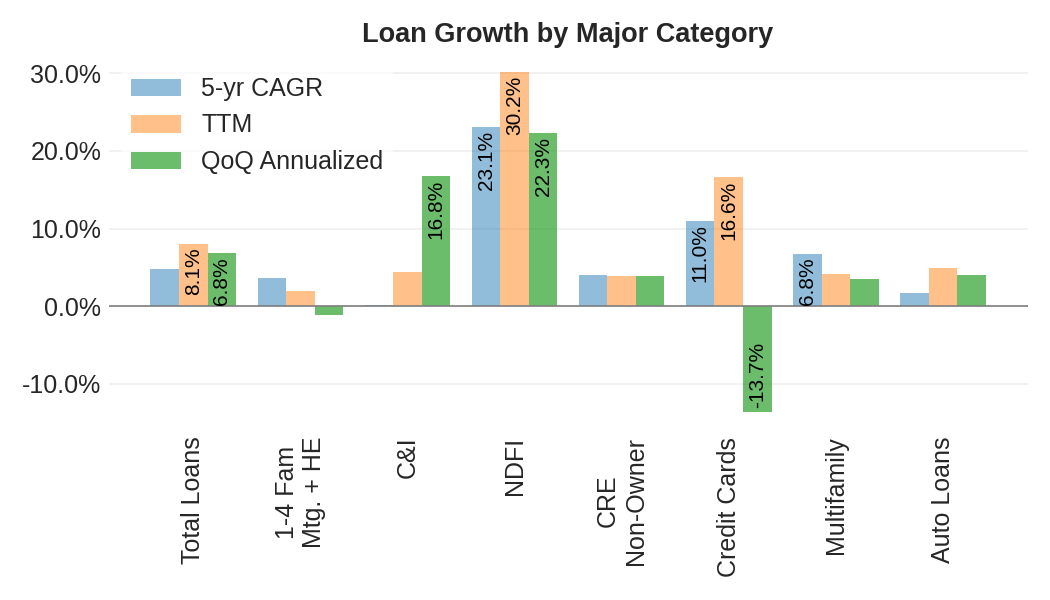

C&I lending emerged as a major growth driver during the quarter as private credit inflows slowed (Exhibit 2). In fact, combined domestic and international C&I lending posted double-digit annualized growth for the quarter, a notable development for one of the largest bank lending categories.

Exhibit 2: C&I Lending Accelerated in Q1

Source: Bankregdata and Cadwalader, Wickersham & Taft LLP.

We see accelerating C&I lending as a durable trend in light of the Basel III proposed revisions that will expand the availability of the 65% risk weight for non-subordinated corporate exposures to investment-grade counterparties to non-publicly traded entities for Category I and II institutions. While C&I lending competes to some extent with for the same bank capital, liquidity, relationship attention, and credit committee bandwidth as fund finance, we also see C&I lending as indirect balance sheet support to the sponsor ecosystem and a positive indicator for commercial credit appetitive that should align with fund finance origination growth.

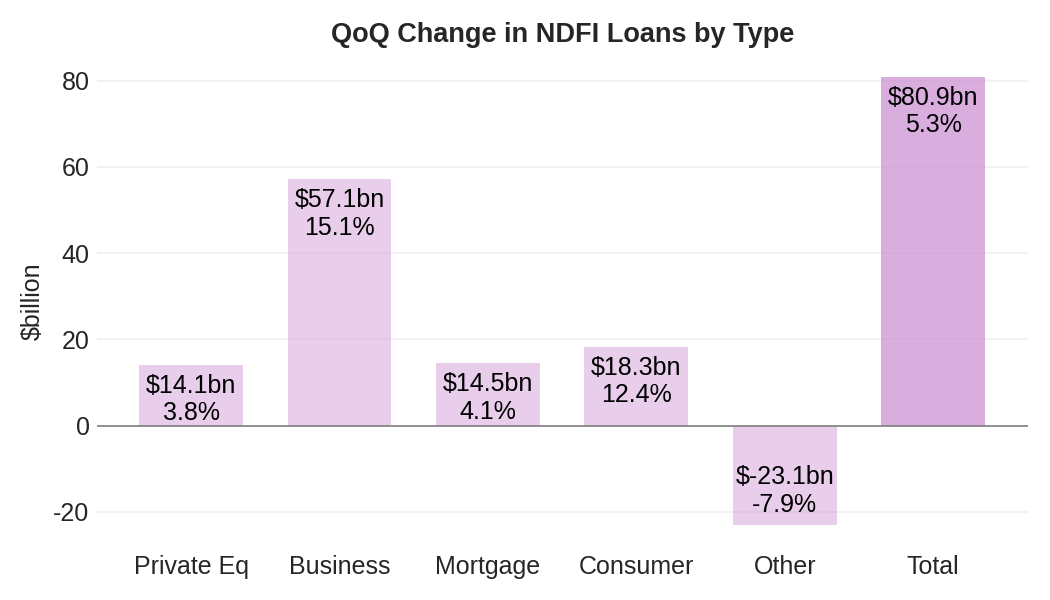

Supporting this read, loans to non-depository financial institutions (NDFIs), where fund finance loans are most commonly classified, posted clear growth. A 2024 rule change for banks with $10 billion or more in assets resulted in loan reclassifications into the NDFI category for several quarters, making changes to loan exposure difficult to interpret and largely resulting in overstated growth. Those reclassifications appear to have been worked through as institution-level NDFI loan growth at an institution level didn’t appear to be matched by large offsetting outflows from another loan category.

Within NDFI sub-categories, loans to private equity increased by 3.8% in the quarter (non-annualized). The most significant growth came from loans to business credit intermediaries, which looks like potential revolver drawdown activity to support private credit liquidity demand (Exhibit 3). (We’ll have to wait to verify this until the FDIC’s Research Information System data is updated for Q1.)

Exhibit 3: Business Credit Intermediary Lending an Outlier in Q1

Source: Bankregdata and Cadwalader, Wickersham & Taft LLP.

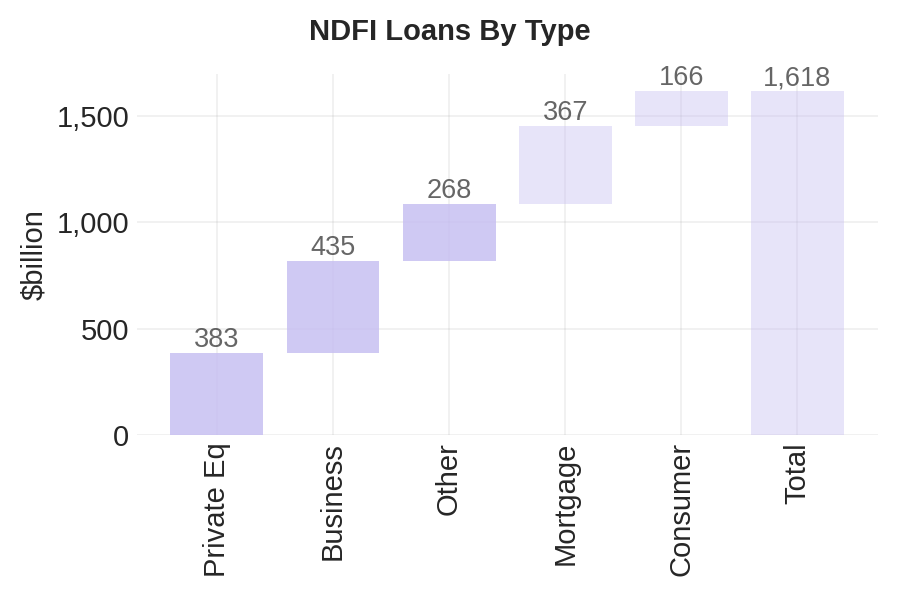

As we’ve previously highlighted, NDFI provides limited information on fund finance lending trends because sub-categories are organized by counterparty rather than product type. Subscription loans, for example, can reasonably be grouped into several of the subtypes (e.g., loans to private equity funds, business credit intermediary or others) and, in the process, mixed in with other loan products. Nonetheless, the continued expansion of the loan category to $1.62 trillion aligns with continued growth in fund finance (Exhibit 4).

Exhibit 4: NDFI Lending Surpasses $1.6 Trillion

Source: Bankregdata and Cadwalader, Wickersham & Taft LLP.

Conclusion

In aggregate, call reports support our view that bank balance sheets retain ample lending capacity to expand lending in 2026, with fund finance continuing to screen well as a relationship product with ancillary fee income, relative value, and clean credit performance. By implication, we see less immediate need for outside capital to the sector. Bank balance sheets will do the heavy lifting in 2026 while off-balance sheet capacity through securitization, term loans, and SRT continue to form a prudent plan for future countercyclical flexibility.