It's time to register for Cadwalader’s annual Finance Forum on October 19 at The Ritz Carlton in Charlotte, North Carolina.

In this article we look at the lender's right to challenge a sponsor’s valuation of their investments in the context of a NAV-backed financing. This right to challenge is a relatively recent development in these transactions, which has come in and out of vogue depending on the general state of the market, with a notable rise at the beginning of the pandemic due to concerns over the accuracy of valuations in the near term.

A fund is a living, breathing organism that aims to achieve much more than being a vessel for a subscription credit facility. The limited partnership agreement of the fund may have to be amended, restated, supplemented or otherwise modified from time to time to address changes in the regulatory environment or legal requirements.

Despite the global syndicated loan market being down 18% for the first half of the year, Cadwalader has surged to the 12th position among all U.S. syndicated loan legal advisors.

Register now!

Cadwalader is proud to sponsor the second annual Charlotte Women in Fund Finance fall forum and networking event. Join us in the Queen City for an exciting and timely panel discussion followed by a networking reception. Additional details to come. You can register here.

All members of the fund finance community are welcome!

In this episode of FFF: Industry Conversations, Cadwalader partner Wes Misson and the Co-Head of Fund Finance at EverBank, Mike Mascia, discuss the recent launch of the Fund Finance division at EverBank, regional bank stress and other industry trends.

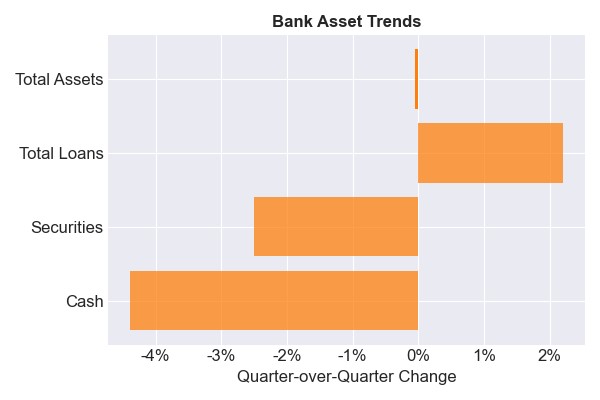

The FDIC set up the SVB bridge bank on March 26, which meant that Q1 bank earnings reports and industry data largely reflected a business environment that had ceased to exist by the time the numbers hit the tape. With the Q2 call report season now largely complete, the new operating environment is becoming clearer.

As we enter back-to-school season and look forward to FFA U this fall, we thought a back-to-basics primer on the limited partnership agreement (the “LPA”), which is the legal and credit cornerstone of our product, would be fitting.

In the continued expansion of its commercial banking operations to provide bespoke and customized fund-level financing to alternative asset managers and the private capital industry, EverBank (temporarily TIAA Bank) announced the launch of its new Fund Finance division this week under the leadership of industry veterans Jeff Johnston and Mike Mascia.