In Part Two of our series on limited recourse finance in the European real estate finance market, we look at the structural features.

Limited recourse structure can be achieved either structurally (which is the most common in real estate financing) or contractually.

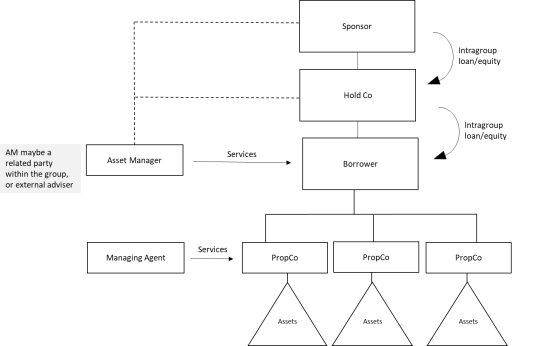

Typical limited recourse borrowing structure

In a typical real estate financing facility, as illustrated in the diagram below, a special purpose vehicle (“SPV”) is set up to be the Borrower and holds the underlying real estate asset; or, in the case of multiple properties, via subsidiary PropCos (each subsidiary again is set up as an SPV, only to hold the real estate asset). The Sponsor provides funding to the Borrower SPV either via an intragroup loan or by equity. A separate management company which is engaged to undertake the maintenance (and sometimes, manage the income such as rent and manage leases and tenants) provides services to the Borrower/PropCos with respect to the properties (“Property Manager”). Often, there is also an asset management company (generally an affiliate of the Sponsor) which provides investment and asset management advice to the Obligor Group with respect to the assets.

To achieve a limited recourse structure, only the Borrower SPV and its subsidiaries will grant security over its assets (which includes the underlying property). The Sponsor and Property Manager will not provide any security over its respective assets, save for assets/rights which are liabilities for the Obligor Group and therefore affect the solvency of the Obligor Group (examples include shareholder loans and claims under management contracts). This will be discussed in more detail in Part Three of this series next month.

Contractual terms to limit recourse – some limitations

Limited recourse can also be achieved contractually by having specific arrangements in place to ensure lenders only have limited claims over certain assets. However, this is often not the preferred approach, as enforcing contractual obligations in situations where the counterparty is not cooperative would require proceedings in court.

Furthermore, in ARM Asset Backed Securities S.A. [2013] EWHC 3351 (Ch), where the sponsor granted a share charge over an SPV, although the share charge provided that recourse to the sponsor is strictly limited to the shares of the SPV whose shares are charged, it did not preclude the Sponsor from being found to be unable to pay its debts and therefore can be wound up. Therefore, this judgment further puts into doubt the effectiveness of limited recourse only via contractual terms.

Clear distinction on assets and liabilities in or out of ring-fenced group

Given the recourse for the lenders is limited to the assets in the security pool and the Obligor Group (which is ring-fenced from the rest of the sponsor group), when conducting due diligence and constructing the security package, additional care needs to be taken to ensure these assets, upon enforcement, will yield sufficient recovery. To this end, in addition to the structural requirements in having all the assets supporting the loan sitting within the ring-fenced structure (or can be easily severed upon enforcement), one other key consideration for lenders is to ensure that liabilities and claims against the ring-fenced group are either contained within the group (i.e., intragroup liabilities) or, if such liabilities are outside of the group (most common example being sponsor debt), such liabilities can be severed in the same way upon enforcement. To the extent there are any liabilities outside of the group which pose as a threat to the lenders’ claim to the debt and/or the assets, such liabilities must be addressed adequately.