In a March 16 hearing before the U.S. Senate Finance Committee, Treasury Secretary Janet Yellen explained that uninsured deposits would be guaranteed only following a determination that “the failure to protect uninsured depositors would create systemic risk and significant economic and financial consequences.” Not surprisingly, given this systemic risk qualifier, deposit uncertainty persists at funds and among institutional bank clients generally, and a move towards severing the lender-depository relationship by borrowing from one institution and maintaining the collateral accounts elsewhere continues.

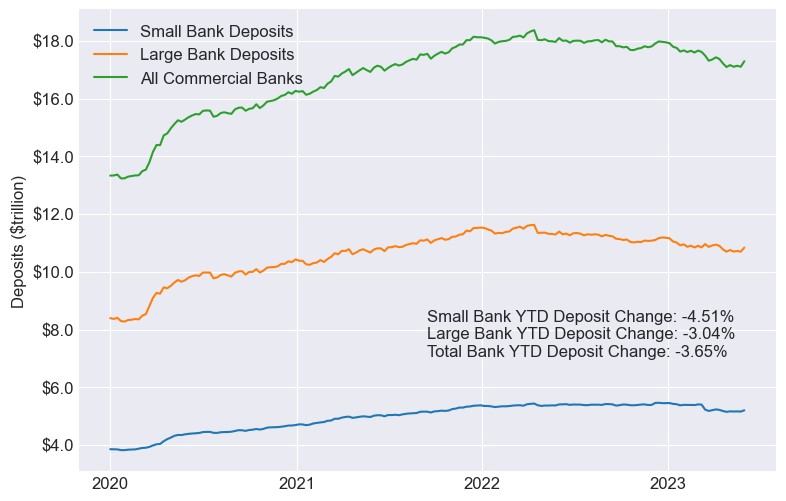

Exhibit 1: Deposits Are Leaving Small Banks Faster

Note: Large banks are defined as the top 25 U.S. commercial banks.

Source: Federal Reserve H.8 Release and Cadwalader, Wickersham & Taft LLP

This deposit alienation trend is problematic at an institutional level but also for the industry as a whole. At the institutional level, a bank originating a loan is adding an asset to its balance sheet. Without the benefit of the associated deposits, the bank now becomes marginally more reliant on higher cost wholesale funding. In addition to the adverse cost-of-funds impact, the natural correlation between its assets and liabilities deteriorates.

There are a few nuances to bring into the discussion. In the fund finance context, deposit duration is short and the institutional impact of losing deposit accounts limited by how quickly funds are cycled out of the collateral account. But if deposit account migration is a broader trend across commercial borrowers and bank verticals, the aggregate institutional impact becomes more material. There is also a credit facet: moving the collateral account to a third party means that enforcement under a cash control event becomes dependent on timely compliance by an outside institution.

This separation of deposits from loans doesn’t affect all institutions equally. Wherever the loan is sourced from, borrower preference is to place deposits at a GSIB. As this plays out over time, the largest banks will continue to gain a competitive advantage by competing for loans from a lower cost funding basis while smaller institutions are left with unequal access to deposits.

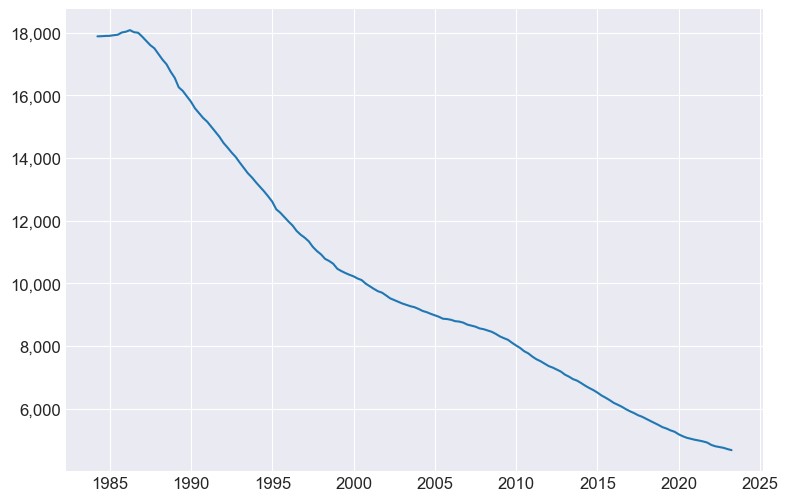

This was already the trajectory in the industry prior the 2023 bank turmoil. In Q1 the top 10 banks held 45% of total U.S. bank deposits. The benefits of scale in a highly regulated industry has for decades driven consolidation and suggests deposits will become more concentrated in the future.

Exhibit 2: Number of FDIC Insured Banks and Savings Institutions

Source: FDIC and Cadwalader, Wickersham & Taft LLP

The good news is that bank lenders can pass along the higher cost of funds to borrowers when deposits are severed from loans. The BHC Act anti-tying provisions provide an exemption for “traditional bank products” such as loans and deposits, meaning that in the event a borrower wanted to house its deposit account at a different institution, the lender would not be prohibited from including a price toggle in the loan documents or otherwise addressing the scenario in its loan terms at origination or amendment.

Of course, there are two sides to the loan transaction. The lender’s approach to deposit alienation has to be one that is palatable to the borrower. From the borrower’s perspective, the risk of loss or delayed access on its uninsured deposits will outweigh a few basis points adjustment in margin. But while the borrower is unlikely to be persuaded to maintain its accounts at the lending institution, the lender doesn’t have to give this right away as a free option to the borrower.

Playing this out over time, the inescapable reality is that institutions with higher cost liabilities will have to make higher interest rate loans. In the fund finance world, pricing has historically been relatively consistent between lenders, with the notable exception of a few prime-indexed lenders. Going forward, it may become increasingly important for non-GSIB lenders to hone a distinctive competitive edge other than price.