We are often asked by clients and non-Irish law firms in the context of fund finance transactions about using fund structures established under the revamped Irish Investment Limited Partnership (“ILP”) regime, and, in particular, how ILPs compare to similar structures in other jurisdictions such as Lux SCSps and Cayman ELPs. We have set out a brief (and hopefully helpful) summary of these matters below.

Background to the revamped ILP Regime

The Irish regime for ILPs was re-designed in early 2021 to ensure that the ILP offers the features expected by managers employing credit, private equity, venture capital and real asset strategies, following successful engagement between industry, the Irish Department of Finance, the Irish Revenue Commissioners and the Central Bank of Ireland (the “Central Bank”). The significance of the re-designed ILP regime has been discussed by Matheson in a previous Fund Finance Friday article, which can be found here. An overview of the key features of ILPs is also set out below.

Why the ILP is proving increasingly attractive to market participants

Ireland is an increasingly popular fund domicile for managers, with managers identifying regulatory conditions (including the speed to market afforded by the Central Bank’s 24-hour authorisation), legal and tax frameworks, and business conditions (such as ease of doing business, service culture and local expertise) as key reasons for this trend. 17 of the top 20 global managers (and over 560 managers in total) have fund operations in Ireland, and 40% of the world’s alternative investment funds (“AIFs”) are administered in Ireland.

More specifically, ILPs offer an Irish limited partner fund structure to managers and other market participants who already deal with limited partnerships in other jurisdictions.

What the increase in popularity of ILPs means for fund finance practitioners

Fund finance practitioners will need to have a solid understanding of the ILP regime in transaction structuring and execution, including with respect to ILP document due diligence, credit support packages and reflecting ILP structures in primary documentation.

The above would, of course, be the case for any fund structure (albeit in relation to the respective regimes of such structures). As such, in practical terms the differences between a financing involving an ILP and an Irish Collective Asset-management vehicle (“ICAV”) or a variable capital investment company will not be drastic for non-Irish fund finance practitioners, with the key distinction being that the transaction will involve limited partnership agreements as opposed to subscription agreements.

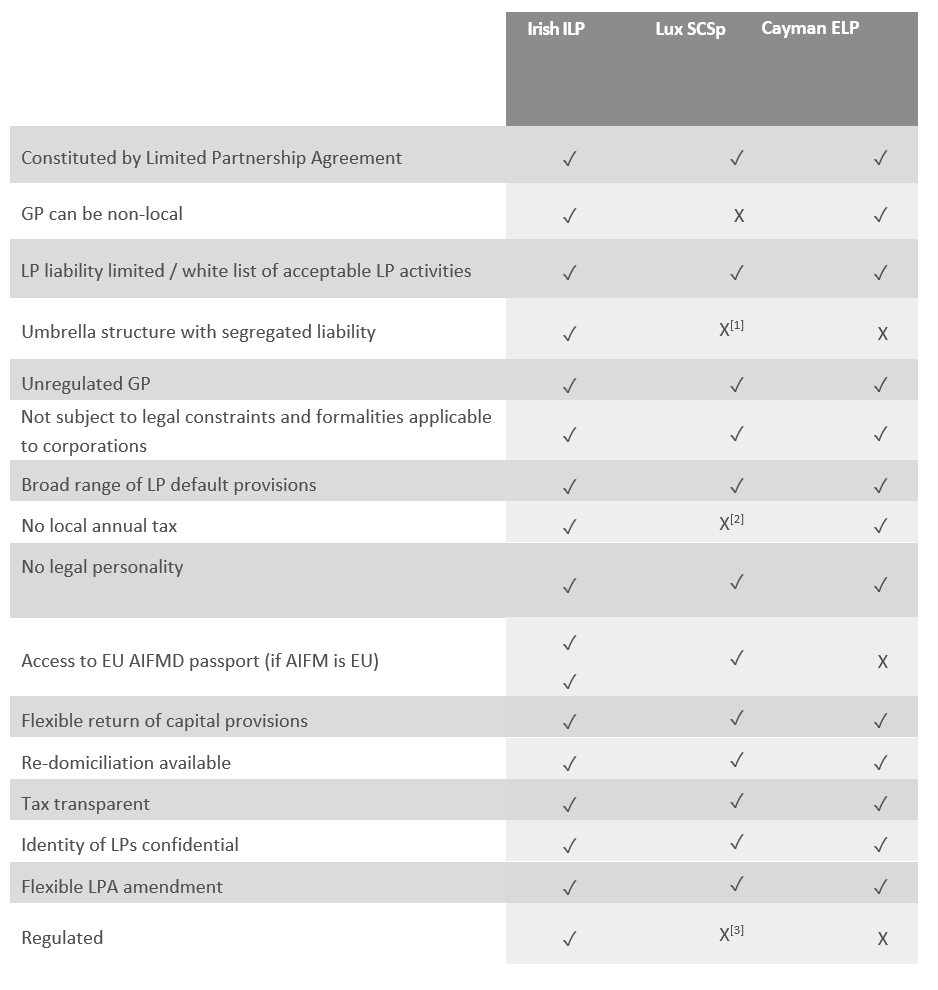

ILPs in comparison to Lux SCSps and Cayman ELPs

As mentioned above, ILPs are increasingly aligned to limited partnership structures commonly used in other jurisdictions. A comparison of the key structural features of ILPs, Lux SCSps and Cayman ELPs is set out in the table below:

- A Lux SCSp can be an umbrella and regulated, but only if it obtains RAIF status.

- A Lux SCSp may be subject to Municipal Business Tax, if it carries out a “commercial activity” or Lux GP owns 5% or more of the SCSp.

- A Lux SCSp can be an umbrella and regulated, but only if it obtains RAIF status.

Overview of the key features of ILPs

Structural Features

- ILPs are regulated AIFs, authorised by the Central Bank and constituted by a limited partnership agreement (“LPA”) with few mandatory provisions.

- An ILP has no separate legal personality, and the general partner (“GP”) is responsible for the management, control and operation of the ILP.

- The GP does not require a separate authorisation from the Central Bank and is not subject to any minimum capital requirements. Directors of the GP (or, where the GP is a partnership, the directors of the general partner of that partnership) must, however, comply with the Central Bank’s Fitness and Probity regime and be approved in advance by the Central Bank.

- The GP can be a corporate entity or partnership, domiciled inside or outside of Ireland.

- Limited partners (“LPs“) can be corporates, natural persons or partnerships. There is no upper limit on the number of LPs that can participate in an ILP and no minimum number either (single investor ILPs are permitted).

- Generally speaking, ILPs have no regulatory limits on leverage (save for loan origination funds). There is no requirement to spread risk – it is possible to have a single asset ILP.

LP Liability

- In general, each LP’s liability is limited to the amount of its capital contribution or commitment to the ILP unless the LP participates in the conduct of the business of an ILP. The ILP Act specifies certain activities (the “white list”) which will be deemed not to constitute participation by an LP in the business of an ILP.

EU Marketing Passport

- Where managed by an EU alternative investment fund manager (“AIFM”), ILPs can be marketed throughout the EU to “professional investors” within the meaning of MiFID II using the AIFMD marketing passport. Where managed by a non-EU AIFM or a registered AIFM, there is no AIFM marketing passport available and it can only be marketed under national private placement rules, where applicable.

Tax

An ILP is transparent for Irish tax purposes. No Irish stamp duty applies to the transfer, exchange or redemption of units in ILPs. An exemption from Irish VAT applies to management and administration services. Ireland has implemented the reverse hybrid rule (“RHR”) under ATAD in a flexible way, such that RHR issues do not arise in the case of tax-exempt investors, investors in nil tax jurisdictions or investors resident in jurisdictions which have a territorial basis of tax. In addition, investors are not automatically considered to be acting together, so an ILP can be established with a small number of investors without triggering any adverse RHR implications. There is also a RHR exemption for widely held and diversified ILPs.

Matheson’s Fund Finance Team

Matheson has advised both lenders and managers in relation to some of the first ILP fund finance transactions to have taken place in the market, and is well placed to advise clients and non-Irish law firms in relation to transactions involving ILPs, or indeed, on any other Irish fund finance transactions. For further information about Matheson’s Fund Finance practice, please see here.

The article was co-authored by Alan Keating, Donal O’Donovan, Finnbahr Boyle, Sherilyn Deane and Turlough Galvin of the Finance and Capital Markets Department at Matheson, alongside Michelle Ridge of the Asset Management and Investment Funds Group at Matheson. For further information, please contact any one of them or your usual Matheson contact.