SMAs are hot in 2025. One of the busiest aspects of our practice this year across many of our lender clients has been subscription facilities for separately managed accounts (“SMAs”). While these deals have been an important part of our practice for a long time, they have a popularity and velocity that we have not seen before, and we are on pace to close the most SMA facilities we have ever closed in a single year in 2025.

By way of background, an SMA is a fund with a single investor. SMAs are generally established as an investment vehicle for a single investor that invests in a specific fund or manager and are tailored to suit the particular needs of such investor. Most SMAs are established by large institutional investors – like a state pension – or large sovereigns. Many of the SMAs we see are established with top-flight, household name sponsors.

SMAs are very appealing to investors who have the desire (and in many cases, need) and wherewithal to invest a substantial amount of capital in a customized way. Oftentimes an SMA will provide an investor with greater control over the investments the fund makes. Given the current geopolitical and regulatory climate, having a degree of control over the types of investments a fund makes is critical to meeting the objectives of many institutional investors and ensuring they stay within the bounds of their investment policies.

SMAs are also incredibly attractive to funds given the current fundraising environment. It is much easier to assemble and close a fund with a single large investor than to aggregate a group of investors to raise a new fund. This is important since fundraising continued its decline in the first half of this year, which continues the trend of a slowing fundraising environment. For example, according to PEI, in 2024, fund count dropped 22% year over year and the total amount raised was down 21%.

While we are still seeing SMAs that invest alongside a main fund, we have seen a trend over the past year where SMAs are established with more perpetual features. This trend is favorable to sponsors and investors alike as it provides meaningful and predictable capital inflows to sponsors (which proves very useful in a tough fundraising environment), while also maintaining flexibility in capital allocation for the investor.

We do think that one should look at that number in the context of some other very large and favorable numbers pertaining to the fund finance market. The addressable market for fund finance now exceeds $15 trillion (which does not include more than $350 billion of evergreen and semi-liquid vehicles like BDCs and interval funds). And, even at this reduced volume, nearly 4,000 funds closed in 2024. Moreover, given the size of the addressable market, we believe that the fund finance market can continue to grow at a fast rate and remain conservatively leveraged. Ultimately, despite a slowdown in fundraising, we in team CWT continue to believe that the long-term growth outlook for fund finance is fully intact. We are seeing that in SMAs and in overall deal origination with our new matters up 24% year over year and 30% above what we saw in 2023, and the year still has a quarter to go.

While SMAs are hot right now, they are definitely not new, and well-seasoned fund finance bankers are very comfortable with the method for approaching them. There was a time when lenders were more cautious about lending to an SMA. That mindset has now evolved and sophisticated lenders are ready and willing to lend to SMAs and will do so with some additional diligence and care and with certain safeguards in place.

The facilities themselves are not much different than a subline for a typical commingled fund. The distinction is that because the borrowing base and collateral package are each based on a single investor, certain terms in the financing documents will be tailored to mitigate the risk posed by a single investor. In particular, the deliverables in the financing will typically include an investor letter that will create privity between the investor and the lender. We do note that in the last several years the strongest sponsors are fending off that requirement or having the investor deliver a less fulsome investor letter. It is also the case that given a single investor forms the borrowing base in an SMA, certain items that would be exclusion events – like failure to timely fund a capital call or a bankruptcy filing by the investor – are sometimes an event of default instead. In terms of best practices when structuring an SMA, here are top considerations to keep in mind. We have also written about best and most protective practices for lenders in these facilities.

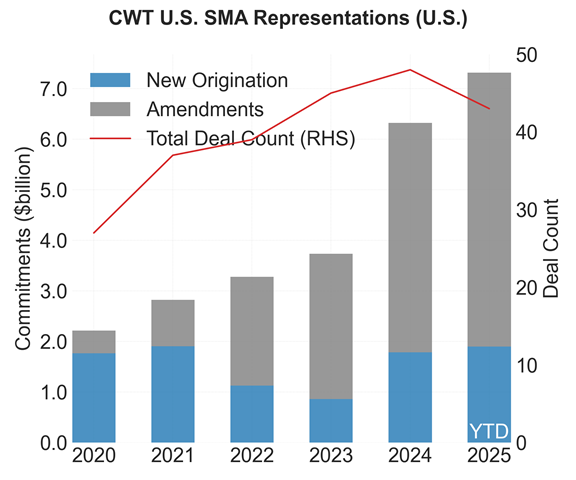

Notwithstanding the fact that fund finance facilities for SMAs require a careful underwrite by the bank and meticulous diligence by the bankers and lawyers involved, these facilities have never been more popular. As many of you know, our group – the largest lender-side fund finance practice in the market – keeps statistics on each deal we close. Given our coverage of a broad swath of the market, we think that our statistics are representative of the market at large. Here is what we are seeing:

- SMA origination is on track for a record year. Our YTD new SMA subscription facility commitments total $1.9bn, which is in line with the full-year 2021 total, with still roughly a quarter to go. We note that current in-flight SMA facilities have commitments totaling in the hundreds of millions.

- These facilities have increased in size over time. New SMA facilities average $119 million in revolving commitments in 2025, which is up from around $100 million in 2020–2023.

- Advance rates are bi-modal with well-funded state pension funds commonly receiving a 90% advance rate while advance rates on other entities range from 50-75%. Lower advance rate facilities most often also price at a higher margin.

- The return of low advance rate facilities (or underwriting of a broader set of investors) is a 2025 theme as only higher-quality investor deals qualified for financing in 2023-2024.

- Margins have been tightening, consistent with the broader subscription market. In the first-half of 2025, we saw high advance rate SMA facilities price around 30-40 bps inside low advance rate facilities.