In this Part 3 of the limited recourse financing series, we discuss some common issues and considerations with respect to the security package in a typical limited recourse structure.

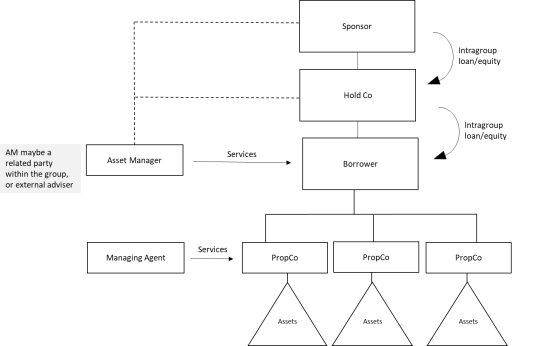

For a typical SPV structure (see diagram below):

The usual English law security package would include all asset security to be granted by all Obligors. The Obligors would include the SPV Borrower and, if the real estate is held by subsidiary PropCos, the shares of such PropCos and also all assets of such PropCos. This will include:

In addition to the security documents, the following documents are generally required:

In considering the security package, the ultimate question for a lender is how the security package should be structured to assist its exit strategy. Clearly, the cleanest, and possibly simplest, approach for a recovery strategy for lenders is to sell the property in an enforcement. Therefore, the approach taken in non-recourse/limited recourse real estate financing would often require security over all assets of the borrower SPV, and each intermediary holding company (if any) to the underlying asset, along with each asset that contributes to generating the cash flow to the property. To ensure the lender can sell off the entire package with relative ease, a share charge is often taken at the holding company level (over the shares of the Borrower SPV, and each of the entities that have property interest) to allow for a corporate sale.

To ensure the security package wouldn’t breach the non-limited recourse structure, security granted by the holding company/sponsor (namely, the share charge and security over shareholder debt, if applicable) must include limited recourse language. The language would provide that the lender's recourse is only limited to the asset subject to security (i.e., the said shares and/or shareholder debt), and beyond these assets, there is no further recourse to the sponsor in any way. Although the documentation seeks to achieve zero recourse/liability against the sponsor by limiting the lender’s recourse only to the assets, the sponsor could, despite the provisions of the security documentation, still be liable. This is the case where there is misrepresentation or breach of covenant on the part of the sponsor involved, as the lender may look to general contractual remedies against the sponsor for breach of contract and seek damages from the sponsor. However, this is distinct to recoveries for the underlying debt owed by the SPV borrower.

Aside from taking security over all relevant assets and cash generating contracts, lenders would ensure that anything which gives rise to liability would be addressed. The types of liabilities can be broadly split into two categories:

Liabilities in the first category would include the head lease (if the property is a leasehold), ongoing maintenance/property management contracts, and, in the case of hotels, the franchise agreement − all of which are essential, and the loss of such contracts and related liabilities would be detrimental to the value of the property.

Liabilities in the second category would include shareholder loans and other subordinated debt, and depending on the nature of the asset management contract and the services provided, if it is determined such services do not contribute to the value and/or cash flow generated by the property, the liabilities under such contracts. It is often the approach to ensure that liabilities classified in category two can be eliminated in enforcement so that the asset is presented in as attractive light as possible to potential buyers.

In Part 4 next month, we will discuss some of the common pitfalls with limited recourse financing structures.

[1] It is often the lenders’ preferred approach to take security over the subordinated debt as it provides proprietary interest over the debt which makes it easier to discharge in an enforcement scenario. That said, in some circumstances where security cannot be provided over the subordinated debt, it is possible to agree to specific powers to write-off the subordinated debt in the subordination agreement. With this approach, the lenders will rely on its contractual rights under the subordination agreement.