July 14, 2022

Like a Netflix thriller or a Robert Ludlum spy novel, we did our best last week to leave our readers in suspense on digital asset jurisdiction and enforcement. While jurisdiction was the big theme last week, the plot thickens this week as authors Peter Malyshev and Michael Ena take a deep dive into enforcement − what's happened to date and what they expect to see in the weeks and months to come. Additionally, as if on cue, a number of regulators gave speeches or released papers and statements on supervision and regulation of crypto-assets, and we provide a quick summary of those statements as well.

Speaking of suspense, we already know the ending of the LIBOR story: the required transition to an alternative rate by the June 30, 2023 deadline. Earlier this week, the Federal Reserve's Alternative Reference Rates Committee (the “ARRC”) published a “Playbook” to provide a roadmap for market participants in transitioning their legacy LIBOR contracts to an alternative rate ... in less than one year. This week, the head of our LIBOR transition team, Lary Stromfeld, explains some of the steps recommended by the ARRC for the successful implementation of fallbacks in legacy LIBOR contracts.

As always, we are very interested in hearing from you. Our market-leading, award-winning LIBOR transition team is ready and able to assist, and we're here to answer any questions about Cabinet News and Views or, more broadly, financial regulatory issues and challenges.

Daniel Meade and Michael Sholem

Co-Editors, Cabinet News and Views

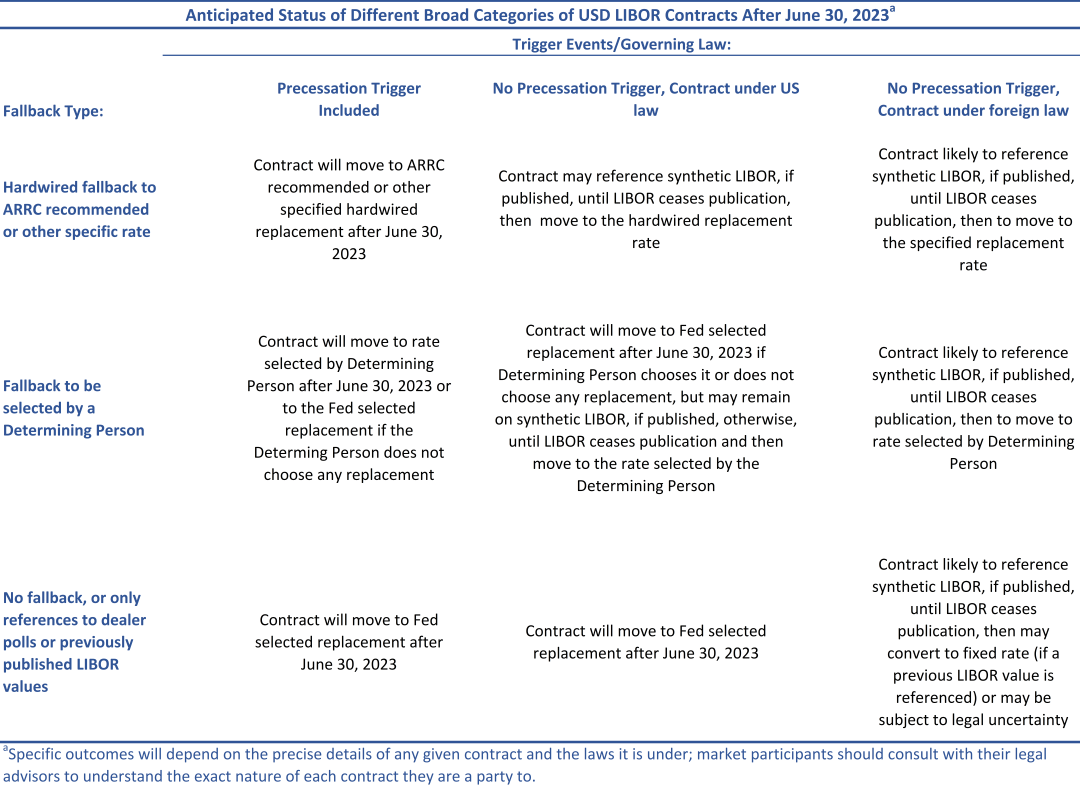

On July 11, the Alternative Reference Rates Committee (the “ARRC”) published a “Playbook” to assist market participants in transitioning their legacy LIBOR contracts to an alternative rate by June 30, 2023. The Playbook describes the following steps that the ARRC recommends for the successful implementation of fallbacks in legacy LIBOR contracts:

- First, if market participants have not yet done so, they should conduct a thorough assessment with their legal counsel of the fallbacks that are embedded (either contractually or through legislation) in every LIBOR contract.

- Because of the large number of contracts that will need to transition, the ARRC continues to encourage remediating those contracts where feasible to reference SOFR before June 30, 2023.

- Finally, for those LIBOR contracts that remain, market participants will then need to adopt plans to communicate each contract’s fallback with the affected parties. They will need to make sure that they have sufficient resources allocated to ensure that these rate changes are successfully put into effect.

Contract Assessment

Focusing on the trigger events, fallback language, and governing law of LIBOR contracts, the Playbook includes a table in which the ARRC depicts, in broad terms, the anticipated status of LIBOR contracts after June 30, 2023 (click or tap for full-size):

The U.K. Financial Conduct Authority (“FCA”) recently published a consultation that seeks market feedback on whether to publish, on a temporary basis, 1-, 3-, or 6-month synthetic USD LIBOR rates. Such a rate, if published, could affect U.S. law contracts that do not contemplate the transition from LIBOR if it becomes “non-representative” (known as “pre-cessation triggers”).

Contract Remediation

The Playbook reiterates the prior guidance from the ARRC and regulators to remediate contracts to move off LIBOR, where feasible, rather than relying upon fallback language of the U.S. federal LIBOR Act. For all remaining contracts, especially business loans, the Playbook advises banks to commit the necessary resources to avoid converting a large number of loan agreements across many borrowers over a short period of time if they do not attempt to work down the stock of LIBOR loans before June 30, 2023. The ARRC also recommended that parties to securities that reference the USD LIBOR ICE Swap Rates strongly consider steps to remediate contracts, including considering the use of buybacks or exchanges.

Fallback Communication and Implementation

The ARRC also emphasized that parties will also need to ensure that the details of the replacement rate and any associated conforming changes are communicated to affected counterparties or investors in an effective and operationally practical manner. The Playbook includes the following best practice recommendations:

- For contracts specifying that a given party (the determining person) will select a replacement rate at their discretion following a LIBOR transition event, that determining person or other specified contractual party should seek to disclose their planned selection to relevant parties at least six months prior to the earlier of either the date that a replacement rate would become effective, or June 30, 2023, using the channels of communication that are available at the time.

- Counterparties to contracts for which a determining person has not disclosed their planned selection at least six months prior to the earlier of either the date that a replacement rate would become effective, or June 30, 2023, should seek to determine whether the party (a) agrees that they serve this role under the terms of the contract, (b) intends to fulfill the responsibility of selecting a replacement rate, and (c) can communicate the nature of the replacement rate they expect to select and when they intend to formally select the replacement rate.

- Determining persons, their agents, or other parties responsible for the dissemination of the change in information regarding LIBOR debt and securitizations should use DTCC’s enhanced LENS system for communicating rate and conforming changes once it is available.

- In addition to ensuring efficient communication of rate changes, lenders should ensure that they have adequate resources on hand to implement the large number of changes that will occur after June 30, 2023.

The last week has seen a number of announcements or statements from financial regulators calling for more oversight of crypto-assets, particularly stablecoins.

Federal Reserve Vice Chair Lael Brainard gave a speech, titled “Crypto-Assets and Decentralized Finance through a Financial Stability Lens,” at a Bank of England Conference on July 8. On July 11, the Financial Stability Board (“FSB”) issued its Statement on International Regulation and Supervision of Crypto-asset Activities. Yesterday, the Committee on Payments and Market Infrastructures (“OICU”) and the Board of the International Organization of Securities Commissions (“IOSCO”), through the Bank for International Settlements (“BIS”) issued guidance on the Application of Principles for Financial Market Infrastructures to stablecoin arrangements.

Vice Chair Brainard’s Speech

In her speech on Friday, Vice Chair Brainard stated her view on the importance “to ensure the regulatory perimeter encompasses crypto finance.” She stated that “the crypto financial system turns out to be susceptible to the same risks that are all too familiar from traditional finance, such as leverage, settlement, opacity and maturity and liquidity transformation,” and thus should be subject to similar regulation and supervision as traditional finance, citing recent losses suffered in numerous stablecoins. Notwithstanding the recent losses, Vice Chair Brainard noted that “the crypto financial system does not yet appear to be so large or so interconnected with the traditional financial system as to pose a systemic risk.”

Vice Chair Brainard also discussed central bank digital currency (“CBDC”). She noted that “there may be an advantage for future financial stability to having a digital native form of safe central bank money …” While she noted that, in the United States, no decision has been made about whether to issue a CBDC, her statement may be the strongest support a member of the Federal Reserve Board has given for a CBDC.

FSB Statement

The July 11 FSB Statement followed a similar theme to Vice Chair Brainard’s speech. The FSB noted that “[t]he recent turmoil in crypto-asset markets highlights the importance of progressing ongoing work of the FSB and the international standard-setting bodies to address the potential financial stability risks posed by the crypto-assets, including so-called stablecoins.” The FSB went on to note that “stablecoins should be captured by robust regulations and supervision of relevant authorities if they are to be adopted as a widely used means of payment or otherwise play an important role in the financial system.” The FSB stated that it will report to the G20 Finance Ministers and Central Bank Governors in October with possible approaches.

OICU-IOSCO Guidance

The OICU-IOSCO report “provides guidance on the application of the Principles for Financial Market Infrastructures (“PFMI”) to stablecoin arrangements (“SAs”) that are considered systemically important financial market infrastructures (“FMIs”), including the entities integral to such arrangements.” The fact that the guidance focuses on how to apply the existing PFMIs to the emergence of stablecoins follows another theme articulated in Vice Chair Brainard’s speech – that like risks should have like regulations. The OICU-IOSCO report highlights four principles from the PFMI that are particularly relevant to stablecoin arrangements: (1) governance; (2) comprehensive risk management; (3) settlement finality; and (4) money settlements.

Yesterday, the full Senate confirmed Michael Barr to a four-year term as Vice Chair for Supervision and to Randal Quarles’ unexpired term as a member of the Board of Governors. That unexpired term as a member of the Board will run until January 2032. The vote for Mr. Barr’s confirmation was 66-28.

As Vice Chair of Supervision, Mr. Barr will lead the Federal Reserve’s bank regulatory and supervision policy-making. Items on the near-term agenda for bank supervision include implementing the so-called Basel III endgame (sometimes also referred to as Basel IV) capital regulations, bank merger policy, ESG efforts, and the bank regulatory approach to crypto-assets.

President Biden, who nominated Mr. Barr in April, stated that the “confirmation of Michael Barr as Vice Chair for Supervision of the Federal Reserve is important progress for my plan to tackle inflation and for sound oversight as we transition to steady and stable growth.”

When Mr. Barr takes his seat, the Federal Reserve Board will have its full complement of seven members.

In last week's Cabinet News and Views, we examined the U.S. regulators' approach to the digital asset space, with a focus on the assertion of jurisdiction by the CFTC, the SEC, prudential regulators, state executive and legislative branches, and Congressional initiatives. This week, our focus shifts to enforcement − what actions the various regulators are taking in the digital asset space and what we can expect to see in the near future.

CFTC Enforcement Actions

Over the past few years, the CFTC brought a number of enforcement actions against participants in the digital asset markets using its regulatory authority over the U.S. commodity derivatives markets, which included allegations of running an unregistered swap execution facility (a “SEF”) and/or designated contract market (a “DCM”) and a derivatives clearing organization (“DCO”), failure to register with the CFTC as a futures commission merchant (an “FCM”), a commodity pool operator (a “CPO”) and/or a commodity trading advisor (a “CTA”), as well as fraud, market manipulation and some other charges. Some of those actions are discussed below. As the CFTC ramped up its enforcement efforts in this area, the amounts of civil monetary penalties imposed by the CFTC increased from nominal in early cases to tens and even hundreds of millions of dollars in more recent cases. Again, as noted above, CFTC’s enforcement actions relate to cases that are clear under the existing authorities, while there are a multitude of instances where it is not clear whether CFTC’s or SEC’s jurisdiction applies (see, e.g., the Department of Justice (the “DOJ”) case involving OpenSea discussed below).

In a number of enforcement actions, among other things, the CFTC alleged that the defendants operated a SEF or DCM that was not registered with the CFTC. For example, in 2015, the CFTC issued an order filing and simultaneously settling charges against Coinflip, Inc., d/b/a Derivabit (“Coinflip”) and its founder, chief executive officer, and controlling person. The CFTC alleged that Coinflip, without being registered as a SEF or DCM, operated an online facility named Derivabit that allowed users to trade standardized U.S. dollar-denominated bitcoin option contracts in violation of Sections 4c(b) and 5h(a)(l) of the CEA and the CFTC Regulations 32.2 and 37.3(a)(l). Coinflip agreed to settle the charges without admitting or denying the findings and conclusions of the CFTC and to cease and desist from future violations of the CEA.

On October 1, 2020, the CFTC filed a complaint against five entities doing business as “BitMEX,” as well as BitMEX’s co-founders, seeking injunctive and other equitable relief, as well as the imposition of civil penalties, for violations of the CEA and CFTC regulations. On August 10, 2021, the CFTC announced that the U.S. District Court for the Southern District of New York entered a consent order against operators of the BitMEX cryptocurrency derivatives trading platform. The court found that BitMEX violated the CEA by operating a facility that offered leveraged trading of cryptocurrency derivatives to, and entering into such transactions with, retail and institutional customers in the U.S. and elsewhere without being approved as a DCM or a SEF. The court also found that BitMEX violated the CEA by accepting Bitcoin as margin for digital asset derivatives and entering into retail commodity transactions without registering as an FCM with the CFTC. In addition, BitMEX failed to implement a customer information program and know-your-customer procedures, and failed to implement an adequate anti-money laundering program. BitMEX was enjoined from future violations of the CEA and ordered to pay $100,000,000 of civil monetary penalties. On May 5, 2022, the court entered consent orders against the three co-founders of BitMEX stemming from the same CFTC complaint. The order required each of the founders to pay a $10 million civil monetary penalty and enjoined them from further violations of the CEA and CFTC regulations. In parallel criminal actions, the three co-founders and one more individual were charged by the U.S. Attorney’s Office for the Southern District of New York with conspiracy to cause, and willfully causing, BitMEX to violate the Bank Secrecy Act in which they pled guilty.

The CFTC also brought a number of enforcement actions alleging that defendants, among other things, illegally offered retail commodity transactions to their customers without being registered as FCMs. For example, in 2016, the CFTC issued an order filing and simultaneously settling charges against an entity where the CFTC alleged that such entity operated an online platform for exchanging and trading cryptocurrencies that offered and allowed entry into retail commodity transactions. According to the CFTC, this entity did not actually deliver cryptocurrencies purchased on a leveraged, margined, or financed basis to its customers who purchased them. Instead, it held those cryptocurrencies on deposit in its own digital wallets (which did not qualify as “actual delivery”). Therefore, the statutory exception under Section 2(c)(2)(D) of the CEA was not available, the retail commodity transactions offered and entered into by this entity were illegal, and off-exchange commodity transactions and this entity failed to register as an FCM in violation of Sections 4(a) and 4(d) of the CEA. The CFTC order required this entity to pay a significant civil monetary penalty and to cease and desist from future violations of the CEA.

On September 29, 2021, the CFTC filed charges against 14 entities. The complaints alleged that 12 of the entities offered to the general public binary options based off the value of commodities, including cryptocurrencies, and encouraged their customers to transfer money or assets to them, without registering as FCMs. The complaints alleged that two of the entities falsely claimed that they were members of the National Futures Association and registered as FCMs with the CFTC.

In another digital asset-related civil enforcement action alleging a failure to register as an FCM filed on May 19, 2022 in the U.S. District Court for the Northern District of Illinois, the CFTC charged Sam Ikkurty (“Ikkurty”) of Portland, Oregon, Ravishankar Avadhanam of Aurora, Illinois, and Jafia LLC, a company Ikkurty owns in Florida, with operating an illegal commodity pool and failing to register as a CPO. In addition, CFTC alleged that the defendants engaged in fraudulent solicitation of at least $44 million for participation interests in certain funds invested in digital assets and other instruments and misappropriated those funds by, among other things, distributing them to other participants in a manner of a Ponzi scheme.

On June 2, 2022, the CFTC filed its first-of-its-kind civil enforcement action against Gemini Trust Company, LLC (“Gemini”), based in New York, for making false or misleading statements or omitting to state material facts to the CFTC in connection with the self-certification of a Bitcoin futures product with respect to, among other things, facts relevant to understanding whether the proposed Bitcoin futures contract would be readily susceptible to manipulation. The proposed Bitcoin futures product was of particular significance since it was to be among the first digital asset futures contracts listed on a DCM and was used by market participants as a pricing source for other financial products referencing Bitcoin.

In a number of other civil enforcement actions, the CFTC also alleged fraud and misappropriation of customers’ funds related to digital assets. For example, in 2019, the CFTC filed a civil enforcement action in the U.S. District Court for the District of Nevada, charging David Gilbert Saffron of Las Vegas, Nevada and Circle Society, Corp., a Nevada corporation, charging the defendants with fraud. The CFTC alleged that the defendants fraudulently solicited and accepted at least $11 million worth of Bitcoin and U.S. dollars to trade off-exchange binary options on foreign currencies and cryptocurrency pairs, among other things. Instead, the defendants misappropriated the funds and used them for other purposes, including making payments to other participants “in the manner of a Ponzi scheme.” On March 29, 2021, the court issued the final order and judgment against the defendants granting a permanent injunctive relief, restitution of $14,841,280 to defrauded pool participants, disgorgement of $15,815,967, and a civil monetary penalty of $1,484,128.

On March 29, 2022, the CFTC announced that the U.S. District Court for the Western District of Texas entered into a consent order in an enforcement action brought by the CFTC against investment firm Kikit & Mess Investments, LLC and its owner. The court found that the firm misappropriated more than $7.2 million from investors who intended to trade forex or cryptocurrency in managed accounts and ordered the defendants to pay restitution, disgorgement and civil monetary penalties.

On May 13, 2022, the CFTC announced that it had filed a civil enforcement action in the U.S. District Court for the Southern District of New York against Eddy Alexandre of Valley Stream, New York, and his company, EminiFX, Inc. where the CFTC alleged that the defendants fraudulently solicited clients to trade cryptocurrencies and other commodities and misappropriated investors’ funds. The CFTC seeks restitution to defrauded investors, disgorgement, civil monetary penalties, permanent trading and registration bans, and a permanent injunction against further violations of the CEA.

On June 30, 2022, the CFTC announced that it has filed a civil enforcement action in the U.S. District Court for the Western District of Texas charging Cornelius Johannes Steynberg and Mirror Trading International Proprietary Limited (“MTI”), a company organized and operated under the laws of the Republic of South Africa, with fraud and registration violations in the largest fraudulent scheme involving Bitcoin ever charged by the CFTC. According to the CFTC, Steynberg created and operated, through MTI, a global foreign currency commodity pool with a value of over $1,733,838,372 that only accepted Bitcoin to purchase a participation in the pool. Steynberg, individually and as the controlling person of MTI, engaged in an international fraudulent multilevel marketing scheme, using the websites and social media, to solicit Bitcoin from members of the public for participation in a commodity pool operated by MTI in the manner of a Ponzi scheme.

SEC Enforcement Actions

Using its exclusive jurisdiction over U.S. public securities markets and financial reporting of public companies, in the recent years, the SEC brought an increasing number of enforcement actions against participants in the digital asset market where the digital assets involved were found by the SEC to be securities or the market participant did not provide an adequate disclosure. The most common alleged violations were unregistered offerings and sales of securities and fraud. Some enforcement actions involved alleged failures to register as an investment company, failures to register as a trading facility, as well as market manipulation. However, the SEC intends to broaden its reach. For example, according to recent reports, the SEC is scrutinizing non-fungible tokens and their trading venues to determine whether any of them are used to raise capital the way traditional securities are used.

Unregistered sale of securities and fraud were perhaps one of the most common grounds for SEC’s enforcement actions relating to digital assets. The SEC brought a number of enforcement actions alleging unregistered sales of digital assets that it considered to be securities. For example, on August 6, 2021, the SEC issued its first order involving securities using the so-called “decentralized finance” (“DeFi”) technology where it charged two Florida men and their Cayman Islands company for unregistered sales of more than $30 million of securities using smart contracts. According to the SEC, the respondents offered and sold digital tokens stating that the tokens would pay interest and profits because investors’ assets would be used to buy income-generating assets. Based on the Howey test, the SEC found that the digital tokens sold by the respondents were investment contracts offered and sold without registration in violation of Sections 5(a) and 5(c) of the Securities Act of 1933. In addition, according to the SEC, the respondents did not buy any income-generating assets with investors’ funds and failed to disclose that to the investors in violation of Section 17(a) of the Securities Act and Section 10(b) of the Securities Exchange Act. The order required the respondents to pay $12,849,354, together with pre-judgment interest, in disgorgement and each of them to pay a $125,000 civil monetary penalty.

In a complaint filed by the SEC on April 28, 2022 in the U.S. District Court for the Southern District of California, the SEC charged three defendants alleging that the defendants offered and sold NSG digital tokens that were securities to the public in an unregistered offering. In addition, the defendants allegedly created an unregistered trading platform for trading NSG digital tokens and engaged in market manipulation schemes by fraudulently creating appearance of trading activity in NSG tokens, making false and misleading claims to investors and misappropriating investors’ funds. The SEC seeks permanent injunctions, disgorgement, with prejudgment interest, and civil penalties against each defendant.

On February 14, 2022, the SEC filed its first-of-its-kind order charging BlockFi Lending LLC (“BlockFi”) with violating the registration provisions of the Investment Company Act of 1940. According to the SEC, BlockFi offered interest-bearing cryptocurrency accounts to retail investors, which SEC found to be securities, without registration and operated as an unregistered investment company because it issued securities and held more than 40% of its total assets (excluding cash), in investment securities, including loans of digital assets to institutional borrowers. In addition, the SEC alleged that BlockFi made false and misleading statements concerning the risk level of its investment product. BlockFi agreed to pay $50 million to the SEC to settle the charges. In addition, it agreed to pay the same amount to 32 states to settle charges of state securities laws violations.

Violations of the anti-touting provisions of the federal securities laws were the focus of the SEC order filed on July 14, 2021. In that order, the SEC alleged that United Kingdom-based Blotics Ltd, the operator of Coinschedule.com, a website that profiled offerings of digital asset securities, violated federal securities laws by failing to disclose the compensation it received from issuers of the digital asset securities it profiled. Blotics has agreed to cease and desist from committing any future violations of the federal securities laws, and to pay $43,000 in disgorgement, plus interest, and a civil penalty of $154,434.

Failure to register as a broker-dealer was charged in a complaint filed by the SEC in the U.S. District Court for the Southern District of New York on August 18, 2020. According to the SEC, two defendants, for a substantial compensation, acted as unregistered brokers in violation of Section 15(a) of the Securities Exchange Act and used social media to promote securities of AirBit Club, an investment scheme that promised high returns through a purported digital asset trading program and from the recruitment of others. Failure to register as a broker-dealer was one of the charges in another complaint filed by the SEC on September 18, 2019, where SEC alleged that ICOBox and its founder Nikolay Evdokimov raised $14 million by conducting an unregistered offering of digital asset securities and acted as unregistered brokers by promoting, offering and selling other digital asset securities for a fee.

A ramp-up of SEC digital asset-related enforcement actions sometimes reaches companies whose core business is not related to digital assets. For example, in an order filed on May 6, 2022 against NVIDIA Corporation (“NVIDIA”), a designer and manufacturer of computer graphics processors, chipsets, and related multimedia software, the SEC alleged that NVIDIA failed to disclose that the use of its gaming processors in cryptomining was a significant factor in the company’s year-over-year revenue growth in violation of Section 13(a) of the Exchange Act and Rule 13a-13 thereunder. NVIDIA agreed to pay $5,500,000 in civil penalties to settle the charges.

Some SEC enforcement actions dealt with an outright fraud committed by the defendants and resulted in parallel criminal charges. For example, in complaints filed by the SEC on April 27, 2022 in the U.S. District Court for the Northern District of California against Bits Capital and David B. Mata, the SEC alleged that the defendants raised almost $1 million from investors based on misrepresentations about an automated digital asset trading bot that was never functional and misappropriated investor’s funds. The SEC seeks an injunction, disgorgement, with prejudgment interest, and a civil monetary penalty. The U.S. Attorney’s Office for the Northern District of California announced parallel criminal charges of wire fraud against the defendants.

On April 21, 2022, the SEC filed a complaint in the U.S. District Court for the Southern District of Florida against MCC International Corp. (“MCC”), its founders and two other entities controlled by them, alleging that the defendants engaged in an unregistered and fraudulent offering of thousands of investment plans called mining packages where the investors were promised to profit from MCC’s operations involving cryptocurrency mining, trading and other activities. The profits were paid to the investors in MCC’s own digital tokens that were to be redeemed on Bitchain, a fake unregistered digital asset trading platform created and managed by the defendants, which in fact prevented investors from redeeming their digital tokens for cash and required them to buy additional mining packages or forfeit their investments. Meanwhile, the defendants misappropriated investors’ funds and used them to fund their lavish lifestyles. On May 6, 2022, the Department of Justice unsealed an indictment charging the CEO of MCC in a $62 million investment fraud scheme.

Another recent complaint alleging unregistered sales of securities in a form of digital assets and fraud was brought by the SEC on March 8, 2022 in the U.S. District Court for the Southern District of New York. According to the SEC, the defendants, John and JonAtina Barksdale engaged in unregistered sales of securities that involved the Ormeus Coin digital token and defrauded thousands of retail investors out of more than $124 million. The defendants used a multi-level marketing campaign, using social media and road shows, making false and misleading statements to promote the offering of Ormeus Coin to investors and sold packages that included Ormeus Coin and an investment into a digital asset trading program. The SEC seeks injunctive relief, disgorgement plus interest, and civil penalties. In parallel, the U.S. Attorney’s Office for the Southern District of New York filed criminal charges against John Barksdale.

Enforcement by the Department of Justice

In the earlier digital asset-related enforcement actions, the DOJ filed parallel complaints when CFTC or SEC investigation uncovered fraudulent activity that warranted criminal charges. On June 1, 2022, however, the United States Attorney for the Southern District of New York and the New York Field Office of the Federal Bureau of Investigation announced an indictment charging Nathaniel Chastain, a former product manager at Ozone Networks, Inc. d/b/a OpenSea (“OpenSea”), with one count of wire fraud and one count of money laundering for using confidential information about NFTs gained from his position at OpenSea to profit from insider trading. To conceal his fraudulent activities, Chastain made his purchases and sales of NFTs through anonymous digital valets and accounts on the OpenSea platform. The charges that Chastain faces carry a maximum sentence of 20 years in prison each. Interestingly, the DOJ did not refer to either the SEC’s or CFTC’s authorities and did not discuss whether a subject matter related to commodities or securities and instead focused on conduct under the federal wire fraud provisions.

State Enforcement Actions

State security regulators also engaged in enforcement actions relating to digital assets. On April 13, 2022, Texas State Securities Board issued an emergency cease and desist order to Sand Vegas Casino Club alleging that Sand Vegas Casino Club and other entities and individuals who were involved in the issuance and sale of more than 12,000 “Gambler” and “Golden Gambler” NFTs to fund a virtual casino business. Purchasers of the NFTs, in addition to various other benefits, were entitled to pro rata shares in profits of the online casinos. According to the order, NFTs were issued and sold without registration of their sale in violation of state securities laws, the issuer failed to disclose material information relating to the NFTs, made misleading statements about profitability of the investment in the NFTs, claimed that the NFTs were not subject to regulation under securities laws and, to confuse investors, used a name and a logo similar to those of Las Vegas Sands Corporation with which it had no association. On the same day, Alabama Securities Commission issued a parallel cease and desist order that contained similar allegations. Both orders alleged that defendants’ acts would cause immediate and irreparable harm to the public. Following the orders, OpenSea, a decentralized NFT trading platform, suspended the sale of Sands Vegas Casino Club’s NFTs.

Over the last year, a number of the securities regulators have issued orders concerning the BlockFi companies’ interest-bearing cryptocurrency accounts. On February 14, 2022, the North American Securities Administrators Association and the SEC jointly announced a settlement with BlockFi Lending, LLC. As alleged by the states, BlockFi promoted to retail investors its interest-bearing accounts for digital assets promising high-interest returns in violation of state registration requirements, which resulted in unregistered sale of securities to the investors without necessary disclosure in violation of state securities laws. BlockFi agreed to pay $100 million to settle the charges and stop offering its cryptocurrency accounts to new investors until its investment product is properly registered. At the same time, BlockFi was allowed to continue to deploy digital assets for its existing investors and pay interest to them. Thirty-two state securities regulators agreed to the terms of the settlement and more jurisdictions were expected to follow.

Conclusion

As many government agencies are ramping up their enforcement activity in the digital asset space, it is difficult to predict the main thrust of the future enforcement actions. However, the recent trend reveals increased attention to stablecoins (especially after the recent demise of the Luna and Terra stablecoins) and NFTs, in addition to the never-ending line of fraud cases. In the absence of a comprehensive regulatory framework for digital assets, in addition to traditional enforcement by the CFTC and the SEC, other federal and state agencies become involved in regulation and enforcement activity with regard to digital assets. The recently proposed industry-friendly “Responsible Financial Innovation Act,” if enacted, may bring more certainty and clarity for the regulators of the digital asset markets and market participants and replace the current regulation by enforcement regime maintained by various government agencies with overlapping jurisdictions.

Cadwalader’s financial services team hosted Part 3 of its four-part series on capital relief trades yesterday.

You can access webinar replays here:

- Part 1: CRT Overview and Regulatory Capital Basics

- Part 2: Unpacking Regulation Q: CRT Structuring

- Part 3: U.S. Legal and Regulatory Considerations

Registration details on Part 4 will follow.