June 4, 2026

Stemming from a case filed in 2022 against the fintech Opportunity Financial, LLC (“OppFi”), the Central District of California issued a decision on May 19 finding that OppFi’s bank partner, FinWise Bank, was the true lender with respect to consumer loans made through their bank-fintech partnership. The California Department of Financial Protection and Innovation (DFPI) is one of several state banking agencies that have sought to establish when a bank actually is a “true lender” for loans that are made, usually to consumers, through programs managed by a bank-fintech partnership. This opinion provides additional insights into what kinds of arrangements in a bank-fintech partnership are necessary to demonstrate that the bank is operating as the true lender, including some useful commentary parsing through the common practice of the fintech recommending loans for approval by the bank and whether that practice usurps the bank’s independence in underwriting loans.

In the partnership between FinWise Bank and OppFi, as described in the opinion, “OppFi’s platform allows banks to provide access to simple short-term lending products for consumers whom traditional lenders may otherwise turn away in light of their credit profile.” Further, “[t]he loan products offered by the Bank provide transparent pricing, have no origination or late fees, are fully amortizing with no balloon payments, and allow borrowers to prepay at any time with no penalty.” These loans have a higher credit risk and therefore “charging higher interest rates is necessary to make small-dollar lending . . . economically viable” and so the banks that want to serve this market are often located in state that “do not set low-interest rate caps relative to credit risk.” In other words, FinWise Bank exports its home-state interest rate into other states, such as California, that have lower interest rate caps.

The DFPI alleged that the arrangement between FinWise Bank and OppFi constituted a “rent-a-charter” arrangement so that the bank “appears on paper to be the ‘lender’ on high interest loans . . . while the non-bank lending company (here, OppFi) performs the actual duties of a real lender such as marketing, underwriting and servicing. [And a]lthough the . . . bank purports to originate the exorbitant interest loan, it immediately sells the loan to the non-banking lending company or the bulk of the receivables.” In other words, DFPI claimed that OppFi was the true lender for these loans and because the loans carried a higher APR than permitted in California, the loans were usurious.

To defend against these charges, the Court describes OppFi’s arguments as being “independently sufficient."

The first argument is that FinWise validly made these loans, demonstrated by all of the following facts: 1) The promissory notes were between the consumer and FinWise; 2) FinWise funded the loans; 3) FinWise held the loans for a couple of days; 4) sold a portion of the loan receivables; 5) held title to the loans for 30, 60 or 180 days after they were funded; 6) assigned a portion of the loan receivables to OppFi; and 7) retained a portion of the loan receivables after fund the loan for 60 or 180 days.

The second argument was that because FinWise was the originator and funder of the loans, and not OppFi, the loans were not subject to the interest rate caps dictated by California law.

The third argument was that FinWise was demonstrably the “true lender” of the loans and was “not a dummy or sham lender.” On this last argument, the court found that FinWise was the true lender for all of the following reasons -- FinWise: 1) controls the application and underwriting processes; 2) independently underwrites the loans and actually rejects some loans that are recommended by OppFi for approval; 3) oversees OppFi’s proprietary credit models; 4) uses is own funds to originate the loans; 5) retains title and ownership of the loans and only sells receivables; 6) gains a financial benefit from the loans; 7) has material risk of loss from the loans; 8) controls the marketing of the loans; and 9) oversees legal compliance of the loans.

In terms of the question regarding whether the loans could be deemed usurious, the Court hearkened back to a 1932 California Supreme Court case that found that the loan “contract must in its inception require a payment of usury or it will not be held” to be usurious and clearly stated that there is no authority for the DFPI’s argument that “the assignee of an exempt lender becomes thereby a usurer” because they are not also exempt. Citing a different California case from 1979, the Court also re-stated that “a contract, not usurious in its inception, does not become usurious by subsequent events.”

The International Organization of Securities Commissions (“IOSCO”) has now published its final report, Recommendations on Valuing Collective Investment Scheme (“CIS”) (the “Recommendations”), which updates and merges previous principles published in 2007 (valuation of hedge fund portfolios) and 2013 (Valuation of Collective Investment Schemes). The Recommendations apply to registered/authorised open-ended funds available to retail investors as mutual funds, including those investing in less liquid, illiquid and hedge funds-like strategies. Unauthorised, non-retail funds and money market funds are out of scope.

IOSCO specifically states that the recommendations are not intended to become good practice for such funds or for such funds to implement them or be assessed against them. The Recommendations are intended to provide a globally relevant framework with the aim of promoting consistent valuation approaches across jurisdictions. They have been updated to reflect recent developments in the market such as the increase in CIS holding less liquid and illiquid assets and lessons learned from periods of market stress and volatility.

The Recommendations are:

- Recommendation 1: The responsible entity should establish comprehensive, documented policies and procedures to govern the valuation of fund assets and ensure an appropriate level of independence in the valuation processes. IOSCO notes that there are substantive changes relating to the addition of effective and independent oversight arrangement of the valuation function and enhanced requirements on governance arrangements under stressed market conditions.

- Recommendation 2: The responsible entity should seek to identify, document, monitor and appropriately manage potential conflicts of interest in the valuation process. Where material conflicts of interest cannot be effectively managed or mitigated, the responsible entity should provide appropriate disclosure in accordance with applicable laws and regulations. IOSCO notes that the main changes related to the disclosure of material conflicts of interest that cannot be effectively managed or mitigated.

- Recommendation 3: The policies and procedures should identify appropriate methodologies that will be used for valuing each type of asset held. The responsible entity should ensure all fund assets are valued at fair value. IOSCO notes that guidance has been enhanced relating to to value fund assets at fair value in line with applicable fund regulations and accounting standards, including elaboration of guidance on back testing and calibration in the valuation process.

- Recommendation 4: The policies and procedures should describe the process for handling and documenting price overrides, including appropriate and proportionate oversight of price overrides.

- Recommendation 5: The assets held or employed by a fund should be consistently valued according to the policies and procedures.

- Recommendation 6: The responsible entity should provide for the periodic review of the valuation policies and procedures to ensure their continued appropriateness and effective implementation. The fund’s valuation policies and procedures should be reviewed at least annually.

- Recommendation 7: The responsible entity should conduct initial and periodic due diligence on third party valuation service providers that are appointed to perform valuation services. The process for the use of third party valuation service providers should be properly documented in the fund’s valuation policies and procedures. IOSCO notes that there are significant new provisions relating to circumstances when third party valuation service providers are used.

- Recommendation 8: The subscription and redemption of an open-ended fund’s units generally should be effected at NAV based on forward pricing.

- Recommendation 9: A fund should be valued on any day that units are subscribed or redeemed, and the responsible entity should ensure that valuations are not stale or inaccurate. Substantive addition of process to address stale or inaccurate valuations.

- Recommendation 10: The fund’s NAV should be available to investors at no fee.

- Recommendation 11: The responsible entity should seek to ensure that arrangements in place for the valuation of the assets in the portfolio and other relevant information are disclosed appropriately to investors in the fund’s offering documents or otherwise made transparent to investors.

- Recommendation 12: A responsible entity should have policies and procedures in place that seek to detect, prevent, and correct pricing errors. Pricing errors that result in a material harm to open-ended fund investors should be addressed promptly, and investors fully compensated. IOSCO notes that guidance on pricing errors and rectification has been enhanced.

- Recommendation 13: The responsible entity should maintain appropriate documentation to demonstrate compliance with their valuation obligations.

Earlier this week, the Federal Reserve Board (FRB) issued its latest semiannual Supervision and Regulation Report. The report delivers a familiar dual narrative for the U.S. banking system: robust headline capitalization paired with an intensifying supervisory focus on specific asset classes and counterparty risks.

The report notes that the banking system remains fundamentally sound, but also signals where examination teams will direct their energy in the coming cycles. For banks, bank holding companies, and their internal legal and compliance teams, the messaging is unambiguous: expect heightened scrutiny of private credit exposures, non-depository financial institution (NDFI) partnerships, and concentrated commercial real estate (CRE) portfolios.

Before diving into systemic vulnerabilities, the FRB highlighted the underlying strength of the traditional banking sector. By most baseline measures, American banking looks highly resilient:

- Over 99% of U.S. banks are well-capitalized by regulatory standards.

- System liquidity remains exceptionally strong, with bank deposits hitting a record $19.5 trillion.

- Large banks posted a 14% return on equity (ROE) in the first quarter of 2026, marking their strongest performance in recent years.

Perhaps the most notable area of developing regulatory focus is the explosive growth of private credit and the banking sector's interconnectedness with NDFIs, such as private equity funds and non-bank credit intermediaries.

The FRB noted that while official regulatory data on non-bank delinquencies currently appears benign, several recent high-profile NDFI defaults have unsettled the sector. Consequently, examiners are closely monitoring how traditional banks are managing their direct and indirect exposures to these private markets.

The report confirms that anticipated headwinds in commercial real estate are persisting, with delinquency rates on CRE loans remaining above their decade-long historical averages. The FRB flagged that the combination of elevated interest rates and depressed property valuations continues to squeeze borrowers' ability to execute favorable refinancings. The supervisory focus remains heavily concentrated on the office and multifamily sectors. Banks with heavy CRE concentrations should expect intensive exam scrutiny regarding their loan workout strategies, internal stress-testing assumptions, and allowance for credit losses (ACL) methodologies.

On the consumer side, the FRB reported a slight increase in loan delinquencies throughout the latter half of 2025 and early 2026, though characterizing the trend as a modest normalization rather than a systemic threat. Delinquencies in auto and credit card portfolios ticked up moderately, but notably finished the year at levels lower than in 2024. While consumer lending remains stable overall, institutions should ensure their fair lending and consumer compliance programs are aligned with their collections and servicing operations.

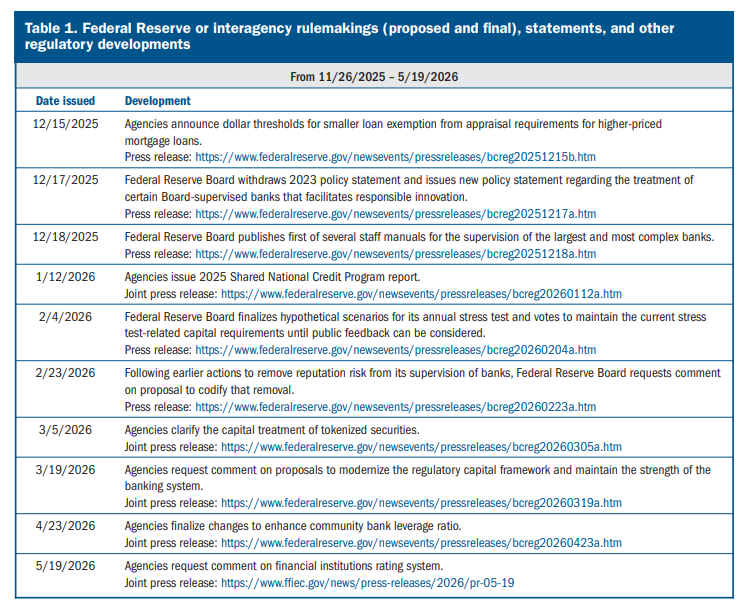

The Report also notes the substantial amount of regulatory rulemaking the FRB, along with the FDIC and OCC have taken since the last report:

The FRB report also notes what Vice Chair Bowman referred to in her Congressional testimony today as supervisory improvements that have resulted in an increase in the number of large banks meeting well-managed criteria, and a reduction in matters requiring attention recorded in exams through focus on material financial risks rather than process.

The June 2026 Supervision and Regulation Report reinforces a supervisory environment where regulators expect institutions to be preemptive, not reactive. Institutions should consider taking the following steps to prepare for upcoming exam cycles:

- Audit NDFI Collateral Frameworks: Reassess margin lending, collateral management, and counterparty credit risk frameworks associated with non-bank financial institutions. If you are relying on dated collateral valuations for private credit counterparties, expect examiner pushback.

- Enhance CRE Stress Testing: Update CRE portfolio stress tests to reflect prolonged higher-rate environments and distressed asset valuations. Ensure that management's workout plans are realistic and actively monitored by the Board.

The overarching theme from the FRB is clear: broad systemic stability will not insulate individual institutions from rigorous supervisory challenges regarding their specific portfolio concentrations and non-bank partnerships.

The Office of the Comptroller of the Currency (OCC) has begun to issue preemption determinations again for the first time since the Dodd-Frank Act went into effect in 2011, a development we explored in our most recent issue of Cabinet. While the determination we discussed last week sought to provide clarity on a national basis regarding which state laws were preempted, the OCC issued a preemption interim final order in April specifically preempting the law in one state, Illinois.

The law in question is the Illinois Interchange Fee Prohibition Act (IL IFPA), which was initially passed in 2024 and was supposed to go into effect July 1, 2025, but now will go into effect, if at all, on July 1, 2027. The IL IFPA is a merchant-friendly law that seeks to do two things: (1) prohibit the charging or receiving of interchange fees on the tax and gratuity portions of payment card transactions by “issuer banks, card networks, acquirer banks, and other participants” (the Interchange Fee Prohibition); and (2) restrict the use of payment card transaction data by any entity other than the merchant (Data Usage Limitation).

The Interchange Fee Prohibition is a logistical and operational nightmare for the payment card industry to implement, with the costs for modifying the system to be in compliance with the IL IFPA dwarfing the benefit to merchants, at least for many years (see the Bank Policy Institute’s amicus brief, here), while also dealing a blow to payment card industry participants by causing them to lose a portion of interchange income forever. In addition, the Data Usage Limitation potentially upends payment card fraud controls managed by banks and the card networks and would most likely make it very difficult for banks to comply with their privacy and security obligations.

The fight over the IL IFPA has been raging in the courts since 2024. A collection of industry trade associations sought to enjoin enforcement of the law, including the American Bankers Association and the Illinois Bankers Association, and in February 2025 the Northern District of Illinois issued a partial permanent injunction barring enforcement of the IL IFPA as against the application of the law to national banks, federal credit unions, federal savings associations, and out-of-state banks operating in the Illinois, as well as the payment card networks. The injunction was appealed to the Seventh Circuit, and upon issuance of the OCC’s preemption determination in April 2026, the Seventh Circuit vacated the permanent injunction and directed that the Northern District needed to assess the impact of the regulatory changes. On June 1, the Northern District issued an opinion and order that effectively ruled that federal law preempts the IL IFPA.

The Court’s decision is important for several reasons, not the least because the OCC’s Interim Final Rule expanded the variety of parties that are impacted by its preemption determination to not only include national banks and federal savings associations, but also the payment networks and interchanges, as well as other parties that “assess, collect, impose, levy, receive, reserve, take or otherwise obtain” a part of interchange “through a fee sharing or similar economic relationship.” The theory there being that due to the economic relationship between banks and these entities, the restrictions imposed on them by the IL IFPA would interfere the banks’ ability to exercise their banking powers. There also is the ticklish issue of whether the OCC’s preemption determinations need to be provided deference by the courts, now that Chevron deference is gone. Chief Judge Virginia Kendall definitely indicated in her opinion and order that she was not bound by the OCC’s actions.

Her analysis concludes that the broadened scope of parties is appropriate and agrees that “in a world where the national banks’ powers will include the discretion to have third parties set their fees for them, it is difficult to see how the [IL IFPA] is not ‘an obstacle to the accomplishment and execution of the full purposes and objectives’ of” national banks’ legitimate powers. In other words, the Interchange Fee Prohibition “is so tied up in the national banks’ powers that the preemptive effect must run to the” payment card networks.

Accordingly, not only has the OCC rendered a preemptive determination on the IL IFPA, but the Northern District of Illinois has permanently enjoined the application of the Interchange Fee Prohibition and the Data Usage Limitation to national banks, banks chartered by states other than Illinois, federal savings associations and the payment card networks. The Data Usage Limitation is also enjoined from being enforced against federal credit unions.

Going forward, the challenge for Illinois legislators will be whether to burden its own institutions with the operational challenges and limitations of the IL IFPA. And, the challenge for the industry will be fending off state laws that are similar to the IL IFPA that are under consideration in state legislatures right now.