Earlier this week, the Federal Reserve Board (FRB) issued its latest semiannual Supervision and Regulation Report. The report delivers a familiar dual narrative for the U.S. banking system: robust headline capitalization paired with an intensifying supervisory focus on specific asset classes and counterparty risks.

The report notes that the banking system remains fundamentally sound, but also signals where examination teams will direct their energy in the coming cycles. For banks, bank holding companies, and their internal legal and compliance teams, the messaging is unambiguous: expect heightened scrutiny of private credit exposures, non-depository financial institution (NDFI) partnerships, and concentrated commercial real estate (CRE) portfolios.

Before diving into systemic vulnerabilities, the FRB highlighted the underlying strength of the traditional banking sector. By most baseline measures, American banking looks highly resilient:

- Over 99% of U.S. banks are well-capitalized by regulatory standards.

- System liquidity remains exceptionally strong, with bank deposits hitting a record $19.5 trillion.

- Large banks posted a 14% return on equity (ROE) in the first quarter of 2026, marking their strongest performance in recent years.

Perhaps the most notable area of developing regulatory focus is the explosive growth of private credit and the banking sector's interconnectedness with NDFIs, such as private equity funds and non-bank credit intermediaries.

The FRB noted that while official regulatory data on non-bank delinquencies currently appears benign, several recent high-profile NDFI defaults have unsettled the sector. Consequently, examiners are closely monitoring how traditional banks are managing their direct and indirect exposures to these private markets.

The report confirms that anticipated headwinds in commercial real estate are persisting, with delinquency rates on CRE loans remaining above their decade-long historical averages. The FRB flagged that the combination of elevated interest rates and depressed property valuations continues to squeeze borrowers' ability to execute favorable refinancings. The supervisory focus remains heavily concentrated on the office and multifamily sectors. Banks with heavy CRE concentrations should expect intensive exam scrutiny regarding their loan workout strategies, internal stress-testing assumptions, and allowance for credit losses (ACL) methodologies.

On the consumer side, the FRB reported a slight increase in loan delinquencies throughout the latter half of 2025 and early 2026, though characterizing the trend as a modest normalization rather than a systemic threat. Delinquencies in auto and credit card portfolios ticked up moderately, but notably finished the year at levels lower than in 2024. While consumer lending remains stable overall, institutions should ensure their fair lending and consumer compliance programs are aligned with their collections and servicing operations.

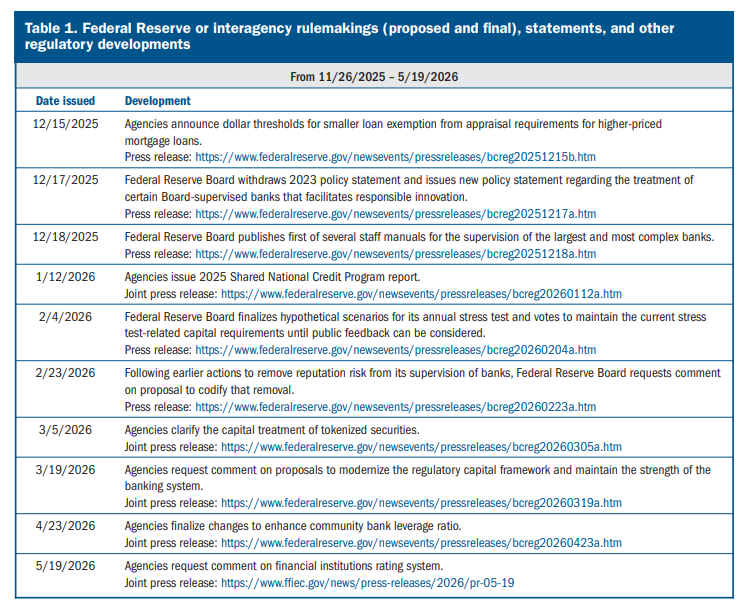

The Report also notes the substantial amount of regulatory rulemaking the FRB, along with the FDIC and OCC have taken since the last report:

The FRB report also notes what Vice Chair Bowman referred to in her Congressional testimony today as supervisory improvements that have resulted in an increase in the number of large banks meeting well-managed criteria, and a reduction in matters requiring attention recorded in exams through focus on material financial risks rather than process.

The June 2026 Supervision and Regulation Report reinforces a supervisory environment where regulators expect institutions to be preemptive, not reactive. Institutions should consider taking the following steps to prepare for upcoming exam cycles:

- Audit NDFI Collateral Frameworks: Reassess margin lending, collateral management, and counterparty credit risk frameworks associated with non-bank financial institutions. If you are relying on dated collateral valuations for private credit counterparties, expect examiner pushback.

- Enhance CRE Stress Testing: Update CRE portfolio stress tests to reflect prolonged higher-rate environments and distressed asset valuations. Ensure that management's workout plans are realistic and actively monitored by the Board.

The overarching theme from the FRB is clear: broad systemic stability will not insulate individual institutions from rigorous supervisory challenges regarding their specific portfolio concentrations and non-bank partnerships.